The crisis caused by the pandemic has forced companies around the globe to rethink the way they work, but even greater changes are just around the corner. What are the takeaways from these challenges, how can we turn them into opportunities and become stronger, and what is the outlook for business?

The findings of a survey by McKinsey & Company do not just reveal some interesting data points but also provide food for thought and insights on the global and individual levels.

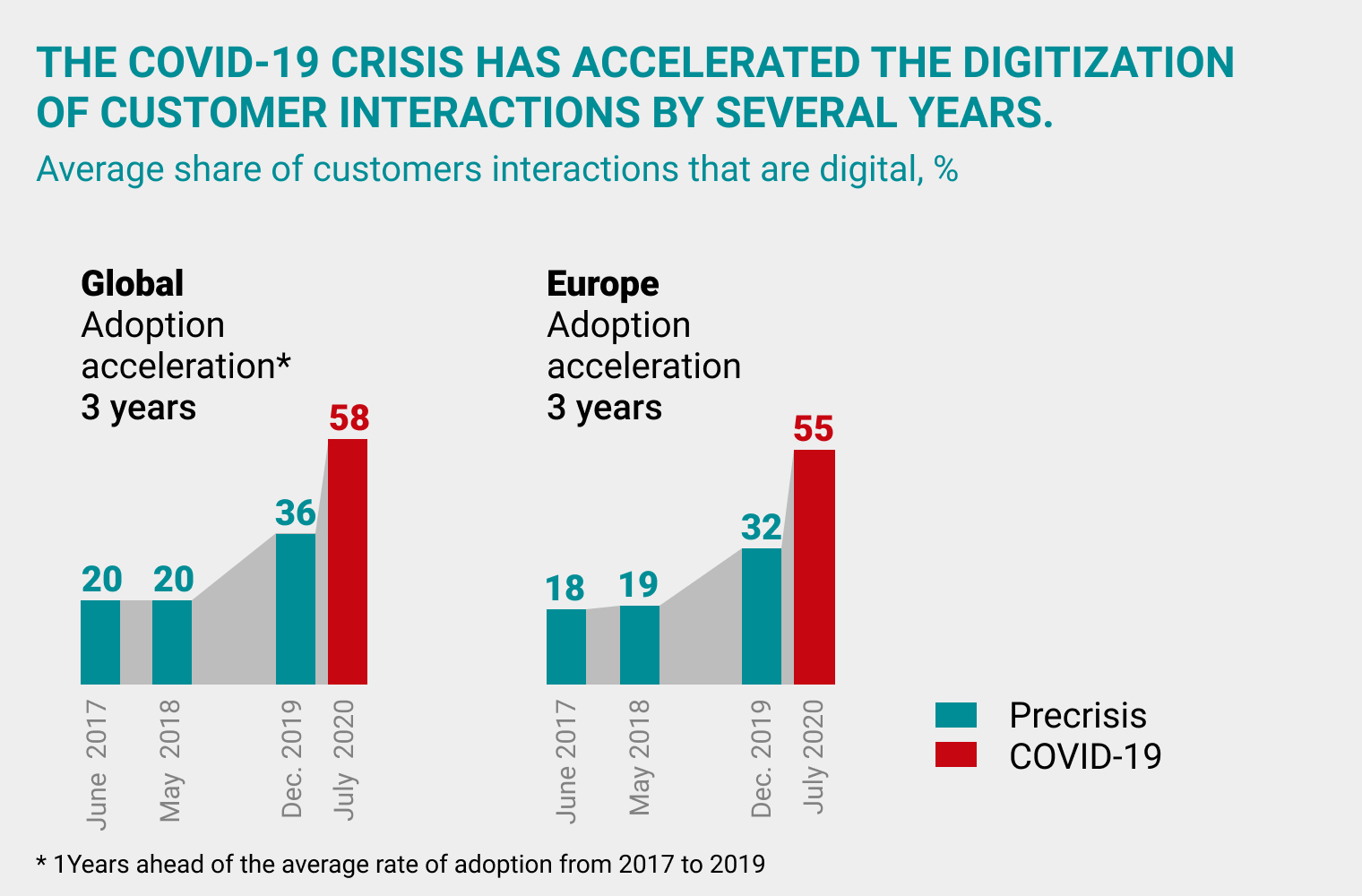

Respondents are three times likelier now than before the crisis to say that at least 80% of their customer interactions are digital

Digital breakthrough

As the crisis unfolded and new needs emerged, many of the stop-gap solutions companies responded with have become long-term solutions that require investment. As corporate leaders point out, spending on digital initiatives has grown the most. According to a global survey conducted by McKinsey (in which 899 top executives and senior managers, fr om an array of industries and regions took part), hundreds of organisations around the world had already accelerated the digitisation of their back-office operations and customer interactions by early summer 2020, reaching their targets three to four years ahead of schedule. Most of them view technology not just as an economic performance driver but also as an essential strategic component of their businesses. These are fast growers that have successfully responded to the crisis, experimented more boldly than others and innovated faster.

Respondents are three times likelier now than before the crisis to say that at least 80% of their customer interactions are digital. Ryan Paulowsky, a partner at McKinsey, has observed that the surge in digitising customer interactions is taking place in every industry, including oil-and-gas and petrochemicals.

“Agile” put in place new working practices and a new operating model, built around the customer and supported by the right processes and governance

The crisis has fundamentally changed how technology’s role is viewed in business and has proved that it is just as important as strong leadership and consistent overall strategy. Three years ago, nearly half of executives ranked cost savings as one of the most important priorities for their digital strategies. Today, more than half of them are investing in technology to gain a competitive edge or are even refocusing their entire businesses around digital technologies. CEOs of companies with falling revenue recognise that they are lagging behind their competitors, including in digitisation, while those who have experimented with, and generously invested in, digital innovation during the crisis are twice as likely to report solid revenue growth when compared to other players.

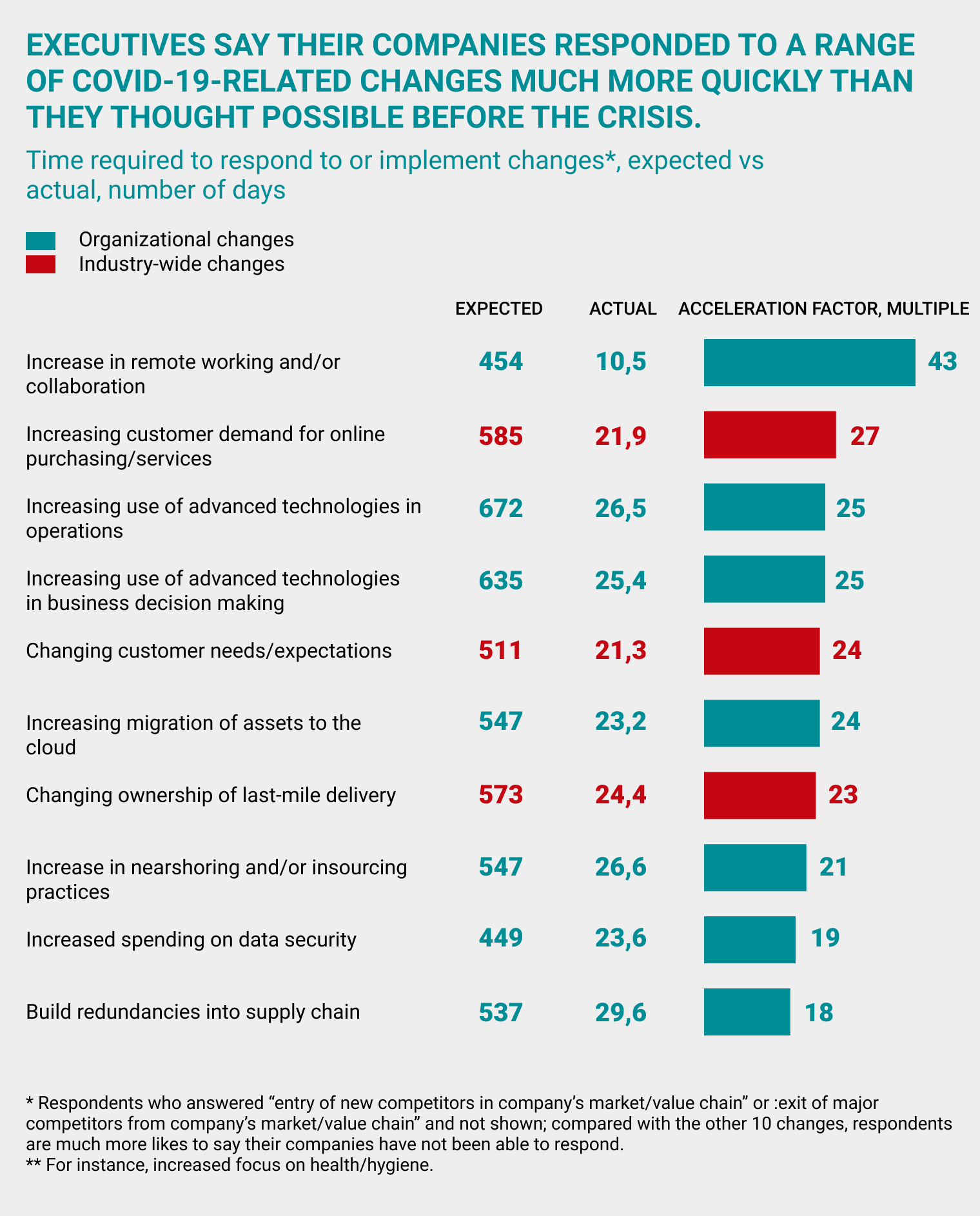

However, the pandemic has also caused other changes besides digitisation. McKinsey asked about important transformations that could or should have happened before the crisis but did not for a plethora of reasons – some changes simply were not a business priority, others raised concerns about consumer resistance or were not feasible due to the lack of IT infrastructure. The speed with which respondents say their companies have responded to a number of changes was faster than their digitisation across the business. For many of these changes, respondents say their companies acted 20 to 25 times faster than expected. At some companies, the shift to remote work was 40 times faster than they thought possible before the pandemic!

The major changes are likely here for the long haul, including the increase in remote work, a stronger focus on health and safety as an emerging customer requirement, changes in supply chains, data security and accelerated migration to the cloud.

Some changes will be temporary depending on margins, business benefits and the ability to meet customer needs. For example, investing in data security and AI helps to position organisations better today than before the crisis.

“Companies must also be prepared for conflict between digital sales channels as they grow,” predicts Ryan Paulowsky. McKinsey experts have already noted that a rapid transition to online customer interactions can cause unintended friction in the process: competition in migrating customer flows between different channels, competition for customers, and a lack of clearly-defined job roles.

The concept for B2B

The COVID-19 pandemic has become a perfect storm in the B2B segment, wh ere business interactions now require speed and accuracy as well as digital and in-person touch points. While many companies had already rethought their sales models, the crisis has accelerated the transformation. McKinsey experts say that over the past year sales situations have changed dramatically, requiring rapid customer responsiveness as well as remote and digital interactions.

8 out of 10 B2B leaders are confident that a multichannel approach is equally or more effective than traditional sales methods. The number of those committed to this approach has increased sharply over the past year – from 54% at the start of the pandemic to 83% in February 2021

In response to changing buying preferences, sales organisations have started moving to become more agile. “Agile” put in place new working practices and a new operating model, built around the customer and supported by the right processes and governance.

Underpinning and enabling the dynamic, fast pace of agile sales teams are the stable practices that provide the structure within which agile teams can operate quickly and effectively. The pre-crisis agile tactics of “doing a scrum” (that is, successive sprints to provide customers with the best possible contact method at every stage and within a short timeframe) have been replaced by “being agile” (which prioritises flexibility at all stages of customer and team interactions). This allows a company to maintain stability, while at the same time creating new sales algorithms, leading to growth.

All the same, as McKinsey experts found during a survey in April 2020 (Two ingredients for successful B2B sales: Agility and stability), mastering traditional ideas of “sales excellence” certainly does not automatically mean the sales team is agile. Learning fr om the experience of global companies showed that, while local sales teams set clear, granular targets, the global business units prioritised other segments and drove innovation with no local market input, so it was impossible for the company to articulate the customer-specific value proposition in time. By the time support was mobilised, customers had already moved on.

Building on the interviews of 2020 and the vast experience of McKinsey in forging agile organisations, the researchers have found that the best B2B sales organisations exhibit five trademarks:

-

Common aspiration across the sales organisation

-

Network of empowered sales teams (supported by digital capabilities)

-

Rapid decisions and dynamic pipeline management

-

Dynamic people support to foster customer-centric sales capabilities

-

Next-generation-enabling technology

McKinsey experts place a particular emphasis on the second trademark: a network of empowered sales teams, supported by digital capabilities.

These teams focus on key account management, in-house sales force and e-commerce tools.

Newly-created key-account customer squads are assigned to a set of customers in a specific sector. The squad is a cross-functional agile team that delivers the entire customer service, from initial contact to post-sales service. Customer representatives interact directly with the different members in the squad, and the key-account manager (also part of the squad) cooperates with the other members daily in a short stand-up meeting, setting the priorities for driving customer satisfaction.

Just as digital-economy companies have powered stock market returns in the past couple of decades, so too could green-technology companies play that role in the coming decades

McKinsey analysts also highlight that the squad also contains dedicated specialists who offer the right operational or content expertise directly to the customer. This personal contact is required when a customer has exhausted all other available information channels. “Bringing the right expertise to the customer at the right stage in the process is crucial to the success of the business,” noted the experts.

Employing a multichannel sales strategy has become more pressing during the crisis, and will likely become essential in the future. Over the past three years, B2B customers’ desire to talk to a sales rep has halved, and more than half of B2B buyers prefer online channels (when B2B buyers want to go digital – and when they don’t). The research suggests that today, 8 out of 10 B2B leaders are confident that a multichannel approach is equally or more effective than traditional sales methods. The number of those committed to this approach has increased sharply over the past year – from 54% at the start of the pandemic to 83% in February 2021.

Moreover, 83% of B2B leaders believe that an omnichannel strategy is a more successful way to prospect and secure new business than traditional ones, despite the high costs and difficulties related to attracting new customers.

Outlook: three methods

As part of their presentation at the Virtual Digital Growth Summit, McKinsey experts distilled their insights from a global survey of 2,500 respondents (representing various industries) into three methods that will drive sales growth in the future: Selling with Insights (using data analytics), Selling with Agility (using agile digital solutions) and Selling with Talent (improving and then applying new and existing skills of managers). The key is to combine all three methods.

In Selling with Insights, analytics is becoming a must-have: over the last five years, the number of analytically driven companies has increased by 50%. Companies surveyed by McKinsey reported that investing in analytics propels growth while data analytics helps predict pricing and reallocate resources against opportunities.

Selling with Agility: Solution selling has become more common across industries, with its effectiveness almost doubled since 2015. Fast growers (83%) are overall more effective at solution selling than slow growers (65%). They leverage digital tools to deliver insights to sales, whereas slow growers focus more on measuring productivity.

Fast growers also benefit from stronger digital and omnichannel presence driven by their investment in virtual capabilities for sales.

Selling with Talent relies on continuously expanding the skill set of sales managers and sales reps while sourcing experts with unique industry experience. Learning programmes are tailored to factor in observed strengths and development areas.

Fast growers excel in consultative selling thanks to negotiating and closing skills, relationship and network building and understanding customer needs.

In another research article – Digital strategy in a time of crisis – McKinsey experts underlined that it’s often the case in human affairs that the greatest lessons emerge from the most devastating times of crises. Companies that can simultaneously attend to and rise above the critical and day-to-day demands of their crisis response can gain unique insights to both better position themselves in the market, and help ensure that their digital future is more robust.

The McKinsey Global Institute estimates that more than 20% of the global workforce could work away from the office – and be just as effective

Looking into the future

Businesses spent much of 2020 scrambling to adapt to extraordinary circumstances, but it is 2021 that will be the year of transition. We have started it looking forward to shaping our future and understanding that there will be no going back to the conditions that prevailed before the pandemic. What trends will shape the next normal, how will they affect the direction of the global economy, how will business and society adjust?

Hope for the future

A global survey conducted by McKinsey and involving 1,382 respondents from various companies, regions and industries, has demonstrated that businesses are quite optimistic about their future. 63% of respondents said that the economic conditions in their respective countries will have improved in 6 months’ time. What’s more, respondents are the likeliest they’ve been in the last three years to expect the global economy’s growth rate to increase, with 68% currently predicting increasing growth.

A consumer rebound

As the efforts to combat the pandemic increase our safety, consumer confidence and spending will return as pent-up demand is unleashed. That has been the experience of all previous economic downturns. One difference, however, is that services have been particularly hard-hit this time. China offers hope: as the first country to be hit by the COVID-19 pandemic, it was also the first to emerge from it. Except for international air travel, Chinese consumers have begun to act and spend largely as they did in pre-crisis times, note McKinsey experts.

How fast confidence will recover is an open question and depends on the country.

A wave of innovation

The tremendous growth seen in digitisation, from online customer service to machine learning to improve operations, has unlocked a world of opportunities for innovation and entrepreneurship. In the third quarter of 2020 alone, there were more than 1.5 million new business applications in the United States – almost double the figure for the same period in 2019. France saw 84,000 new business formations in October, the highest ever recorded. Germany, Japan and Britain have also seen an increase in new businesses compared with prior periods. McKinsey has not yet applied its expertise to this issue in Russia, but Ryan Paulowski believes that the way new businesses are emerging in the country differs significantly from what is happening in European countries.

According to data provided by the Federal Tax Service, the number of micro, small and medium-sized enterprises stood at 5.7 million as at 10 December 2020. A month earlier, the number was 5.6 million. In the wake of the first wave of the pandemic, the number of SMEs fell dramatically, and is only slowly recovering.

Changes in shopping behaviour

Selling requires the development of new skills, capabilities, and business and pricing models. Overall digital adoption is almost universal, even in countries that had been cautious about shopping online prior to the COVID-19 crisis. Consumers are moving online. To reach them and gain their loyalty, companies have to go there, too.

63% of respondents say the economic conditions in their countries would be better six months from when they took the survey

Industry 4.0

The role of technology in life and in business will continue to grow. Many executives reported that they moved 20 to 25 times faster than they thought possible on the adoption of IT tools. In the past, it has taken a decade or longer for game-changing technologies to evolve from cool new things to productivity drivers. The COVID-19 crisis has sped up that transition in areas such as AI and digitisation by several years, and companies now need to institutionalise what has been done so far.

Supply chains rebalance

As much as a quarter of global goods exports could shift by 2025. The COVID-19 pandemic revealed vulnerabilities in supply chains, when even a single factory going dark shut down production. Once businesses began to study how their supply chains worked, they realised that such shocks are predictable features of doing business that need to be managed like any other, and are often caused by the lack of understanding of what is going on lower down in their supply chains. With the development of AI and data analytics, companies can change the situation.

The future of work

During the pandemic, tens of millions of people transitioned to working from home – that is a once-in-several-generations change. It’s happening because advances in automation and digitisation made it possible. The McKinsey Global Institute estimates that more than 20% of the global workforce could work away from the office – and be just as effective. However, there are two important challenges related to the transition to remote working. One is to decide the role of the office itself in business and corporate culture and improve it to meet the new safety requirements. The other challenge has to do with adapting the workforce to the requirements of automation and digitisation, which requires reskilling, upskilling and inculcating a culture of lifelong learning.

Green economy

The need for environmental sustainability is recognised all over the world. Countries are investing in green energy to address climate change, while businesses need to respond to the sustainability concerns of investors by taking action to lim it their climate risks. Just as digital-economy companies have powered stock market returns in the past couple of decades, so too could green-technology companies play that role in the coming decades.

“We still need to research the factors which will affect Russia’s economic and social future, but we are confident that the aforementioned trends will resonate throughout the world, and Russia will be no exception. The country’s transition towards a green economy may differ in pace from the rest of the world. On balance, however, other sources of change are relevant for Russia as well,” concludes Ryan Paulowski.

Necessary changes

The fast-track development of SARS-CoV-2 vaccines is an example of the potential of medical innovations and the actual bio revolution, which goes well beyond health. As much as 60% of the physical inputs to the global economy could theoretically be produced biologically. Examples include agriculture, energy and materials.

Learning from the experiences associated with the pandemic can show the way to build stronger healthcare systems, provided that governments across the globe take forward-thinking efforts, with an emphasis on turning the painful lessons of COVID-19 into effective action.

Being better prepared for the next pandemic and investing in prevention and public-health capabilities have to be a high priority. Employers should take the opportunity to build healthier work environments and invest effectively in employee health.

People who travel for leisure and pleasure are tired of closed borders and will want to get back to doing what they love. Business travel, however, might face long-term structural changes. The pandemic has shown how effective technology can be in addressing business matters, with video calls and so on. What’s more, faced with economic constraints, companies will have to revise their international travel spending. Business-travel managers expect business-travel spending in 2021 will only be half that of 2019.

Download PDF