Note to readers

Peter O’Brien, Member of the Management Board – Managing Director for Economics and Finance at SIBUR.

Crisis management plan: Agile + Digital

A survey by McKinsey & Company confirms that digital solutions underpin successful transformation towards the new economy.

A turbulent year with good results

In an interview with TV channel Russia-24, Mikhail Karisalov spoke about the 2020 results.

SIBUR AND SINOPEC: AGCC DEAL CLOSED

The deal will give joint control over the JV to the two parties.

A case study in effective management

Dmitry Konov has addressed the participants of the Leaders of Russia national management competition.

SIBUR PolyLab receives accreditation

Laboratory test certificates now carry the Combined ILAC MRA Mark.

A green packaging solution

SIBUR, O3 and Jokey launch a production line that will use packaging containing recycled plastic waste.

SIBUR’s environmental successes

The Company’s efforts in ESG risk management and the use of eco-friendly production practices.

SIBUR-Neftekhim’s modernisation drive

SIBUR’s Dzerzhinsk site has expanded its monoethylene glycol production capacity to 830 tonnes per day.

“Plarus” upgraded equipment

«Europlast» Enterprise Association Plant will increase the production of secondary PET packaging recognition shop by 30 tons per day.

CLEAN AIR AT SIBUR PLANT

An air purification unit has been launched at Voronezhsintezkauchuk.

Business needs an open economy

Dmitry Konov took part in an expert discussion dedicated to Russian foreign economic development at the Gaidar Forum.

INTERLAKOKRASKA 2021

For the first time since lockdown, manufacturers of paint and coating materials, raw materials and equipment met in person to exchange news and discuss the situation in the industry.

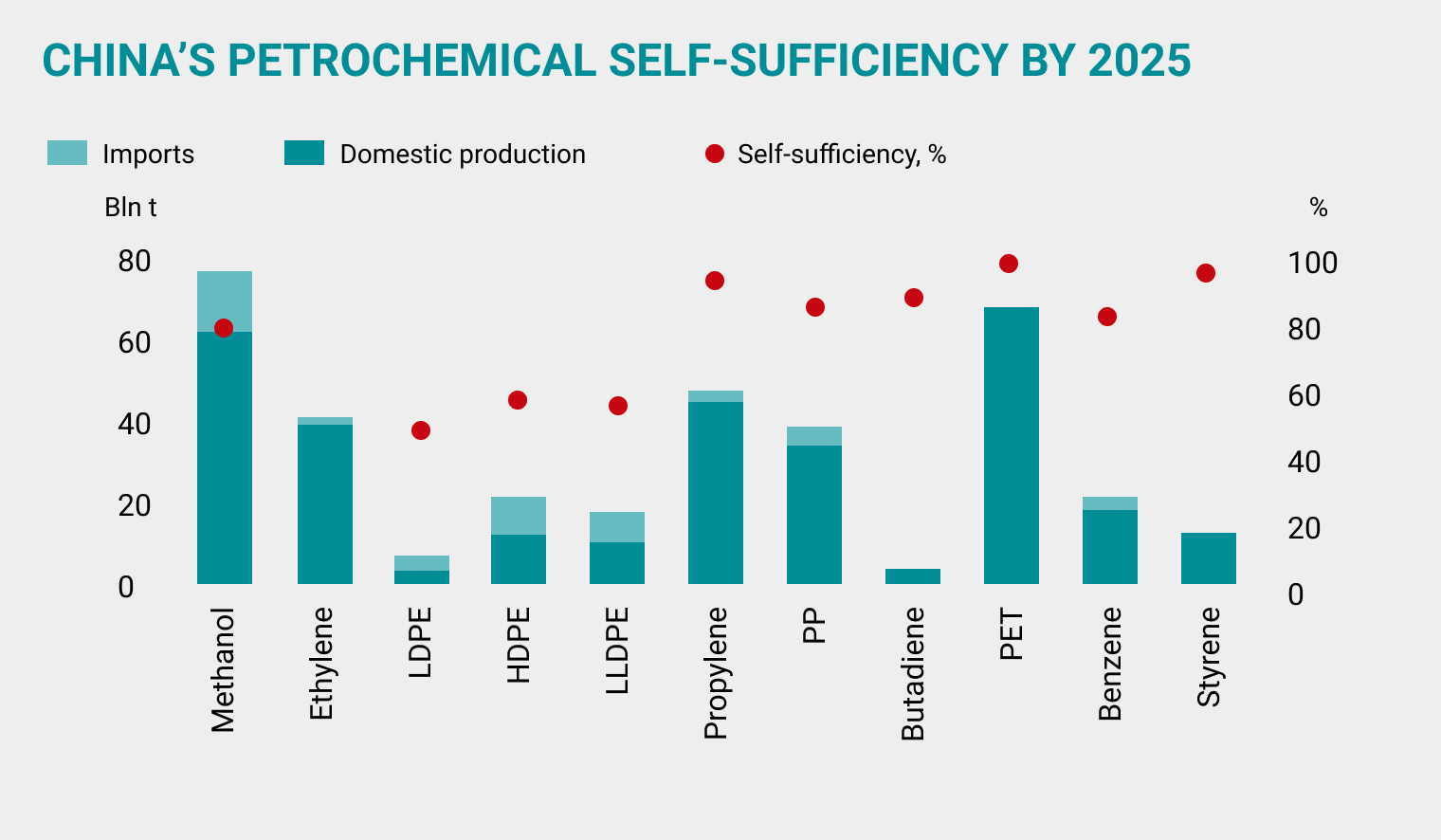

China to lead global propylene capacity

China will contribute 48% to the global propylene capacity additions by 2030.

Sustainable Development and ESG Indices

Head of Environment Galina Khristoforova spoke about introducing a sustainability strategy at the Company.

Research results

According to the annual survey results our clients commended their interaction with SIBUR.

A rally on the polymer market

Prices of plastics have risen following a recovery in the market and growth in global prices.

Plastic in 2021: consumption outlook

The pandemic has badly affected consumption of polymer products, but this year demand will see a return to growth.

SIBUR’s export market strategy

Interview with Andrey Frolov, Executive Director of SIBUR International.

SIBUR analytics

Experts from SIBUR’s Investment Planning and IR division review the results of 2020 and give their forecasts for 2021.

SIBUR International in China: growing stronger

SIBUR International team’s inherent readiness for challenges allowed them to survive a deep transformation.

Plastics reuse and recycling

SIBUR and its partners are leading the recycled plastic charge.

WEF: looking ahead

The World Economic Forum gathered to discuss the major economic and social challenges for the years ahead.

A jab for the economy

Exactly how the world economy recovers will be the driving force behind the level of demand for petrochemical products in 2021.

Digital Chemistry

How digital tools are taking business to a new level.

Trends in the packaging market in 2021

Development trends in the Russian and international packaging market were discussed on the similarly-named SIBUR Business Practices webinar platform.

The BOPP market in 2020

The impact of the pandemic, consumer expectations on packaging, and trends in Russia’s BOPP film sector were discussed at a round table event.

The Rubber Market: from Crisis to Growth

Having survived the shake-up of the industry in 2020, rubber manufacturers expect the global market to recover and hope for state support.

SBS polymers in the adhesives industry

COVID-19 and the eco trend are impacting on the adhesives industry.

CSR: Investment in the future

Russian companies are increasingly investing in corporate social responsibility.

SIBUR’s new Counterparty Code of Business Conduct

SIBUR has introduced a new document that strengthens the way it interacts with partners.

Fantastic Plastic

Moscow Design Museum’s Fantastic Plastic exhibition showcases 13 designer products made of recycled waste.

BASF and SIBUR: A Model Partnership

Christoph Roehrig, Head of BASF in Russia and CIS: the global chemicals giant and SIBUR are joining forces for their sustainable development.

RCU: “We stand for conscious consumption”

An interview with Maria Ivanova, First Vice-President of the Russian Chemists Union.

The polymer pipe market

Representatives of POLYPLASTIC Group shared their views on the scope for polymer pipe product use in the oil and gas industry.

Innovation in response to the pandemic

International Plastic Guide is introducing advanced technologies and developing new products.

“We export about 40% of our production”

Vadim Babij, Owner and Managing Director, Padana Chemical Compounds, talks about the evolution of his company and working with SIBUR.

To achieve a goal, you must change the world

Sergey Grinko, Director, Production Support, talks about “breaking the mould”, craving adventure, and the ability to be happy.

Mentoring: Between Shadowing and Coaching

The advantages of mentoring within a modern company.

Trends in Human Resources

Eight new trends that will shape business in 2021.

The right to leadership

Five ways to be more confident and humblebrag at work.

Employees are in need of training

Almost a half of employees at Russian companies are underqualified.

A guide to service design

A new method for service design has created unique competitive advantages.

Back to the office

According to a survey by HeadHunter, 22% of employees in Russia say they are willing to get vaccinated to be able to go back to work.

Adapting to the aftermath of the pandemic

PwC and Deloitte: Russian executives have revised their strategies in the face of COVID restrictions.

The workday has become longer since the pandemic

Since shifting to work from home, Muscovites have been working up to ten hours a day.

TOP MANAGERS TAKING QUESTIONS

In the Q&As section, our top managers answer the most interesting and relevant questions from our clients sent to dearcustomer@sibur.ru.