To the reader

by Oleg Makarov, member of SIBUR’s Management Board and Executive Director.

From products to services

Rapid technological advancement and changing consumer behaviour urge businesses to expand their service proposition and reinvent customer support. In this context, SIBUR held a workshop in the Tver Region on customer relations and marketing and sales (M&S) development.

World Cup on the money

SIBUR supplies polymers for special banknotes celebrating the FIFA World Cup.

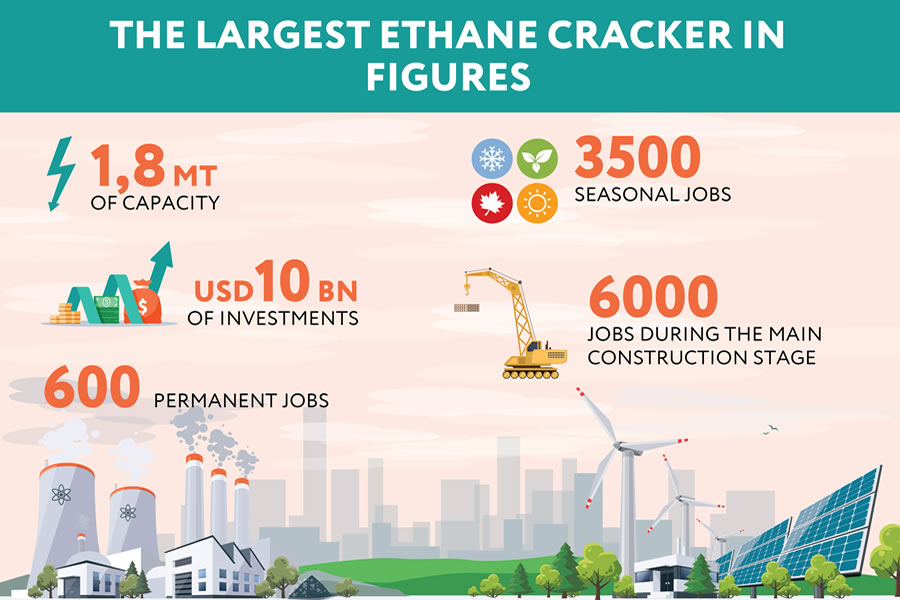

Driving growth in the Far East

SIBUR and Gazprom signed an agreement to supply ethane to the Amur GCC.

Media day in London

SIBUR held a media day in London to reach out to the world’s leading business and trade media and news agencies.

Launching pad for exports

SIBUR plans to bring forward several new grades following the launch of ZapSibNeftekhim.

Domestically produced

SIBUR and equipment manufacturers announce the results of import substitution efforts.

New copolymer rubber

SIBUR's Togliatti site expands the range of copolymer rubber grades.

IISRP meeting in Madrid

The International Institute of Synthetic Rubber Producers holds its annual meeting in May

Chemistry-themed stand-up

Moscow hosts Science Slam, a science battle staged by SIBUR.

Origami made of polymers

Scientists have developed a composite polymer to 3D print self-folding structures.

Firm leadership

HeadHunter names SIBUR Russia’s best employer for a second time.

"A" rated supplier

Bridgestone tyre manufacturer confirms SIBUR as reliable supplier.

Sports fever

The 2018 FIFA World Cup in Russia drove a rise in demand for synthetic materials used in the construction and improvement of sports infrastructure.

Healthcare of the future

Fast-developing healthcare and related technologies pose a serious challenge to petrochemical companies.

SHIFTING THE INDUSTRY FOCUS

The migration of petrochemical manufacturing from the Middle East to the U.S. Gulf Coast.

Business in Turkey

Sergey Grebenev, Head of SIBUR International in Turkey, talks about the Turkish business style.

Investing in the future

We take a focus on the Company 's educational partnership with schools and universities.

New champions

SIBUR supported CASE-IN, an international engineering championship.

Freight village in Vorsino

We take a look at the Vorsino Industrial Park, where SIBUR is involved in developing a logistics hub.

“Excellence in everything”

Maxim Yurov, CEO at RosTurPlast, on how to grow by 30% a year and benefit from sanctions.

Exploring life

Andrey Frolov, Sales Director of SIBUR's Plastics, Elastomers and Organic Synthesis Division, shares his thoughts on sports, love and balance in life.

TOP MANAGERS TAKING QUESTIONS

In the Q&As section, our top managers answer the most interesting and relevant questions from our clients sent to dearcustomer@sibur.ru.