Opening the event, Pavel Gusev, Head of SIBUR’s Plastics, Organic Synthesis and Fuel Components, stressed that this is not a new communication format for the Company. Since the start of the coronavirus pandemic, SIBUR has actively used virtual formats to reach out to partners and customers. “The situation has required us to collaborate in finding answers to questions that proved to be relevant. And what is happening in the market is not always just negative. Crisis is a time when new trends emerge, which means the situation needs to be analysed fr om different perspectives,” said Pavel Gusev.

2020 is a very difficult year, not only in terms of impacts, but also given the uncertainty that still exists today

Trends in key markets

Alexander Shkulin, Head of Analysis and Market Research at Refinitiv, shared his view on the current situation in global markets. “Today, the motor fuel market is clearly following the trajectory of the overall coronavirus situation and oil prices. 2020 is obviously a very difficult year, not only in terms of impacts, but also given the uncertainty that still exists today,” Alexander believes.

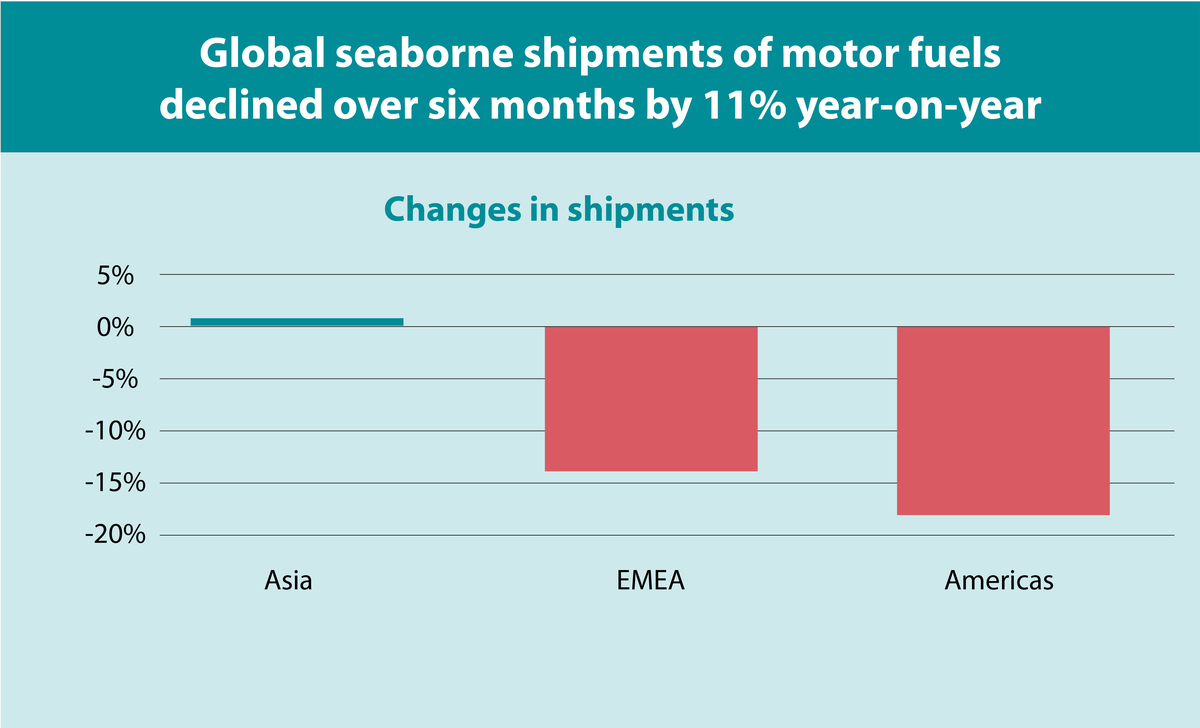

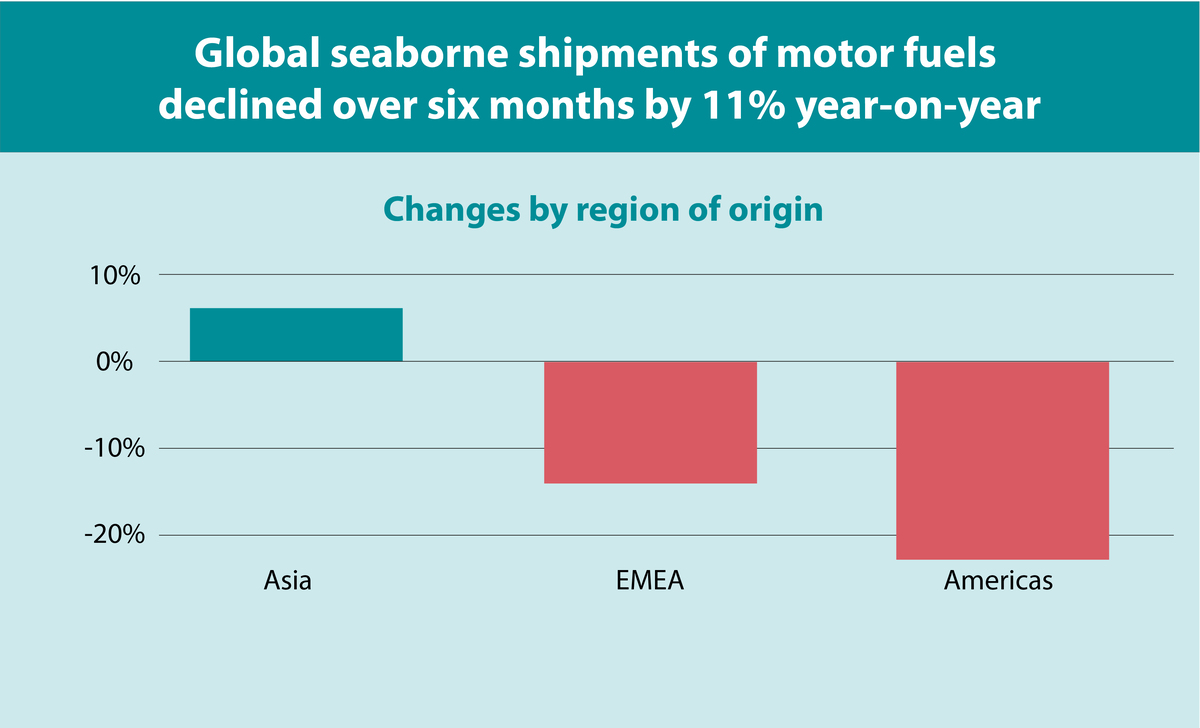

Analysing the global trade in petroleum products through an assessment of merchant marine fleet operations over the past six months, Refinitiv experts recorded a global decline of 11% in gasoline, diesel and gasoil shipments. The biggest fall was in Q2. The gasoline segment was the hardest hit, dropping 15% on the back of lower demand for fuel fr om car owners, with diesel fuels falling a little less. This downward trend has been observed in all regions of the world, with the exception of Asia, which was the first to be hit by the pandemic and emerged from lockdown sooner than others.

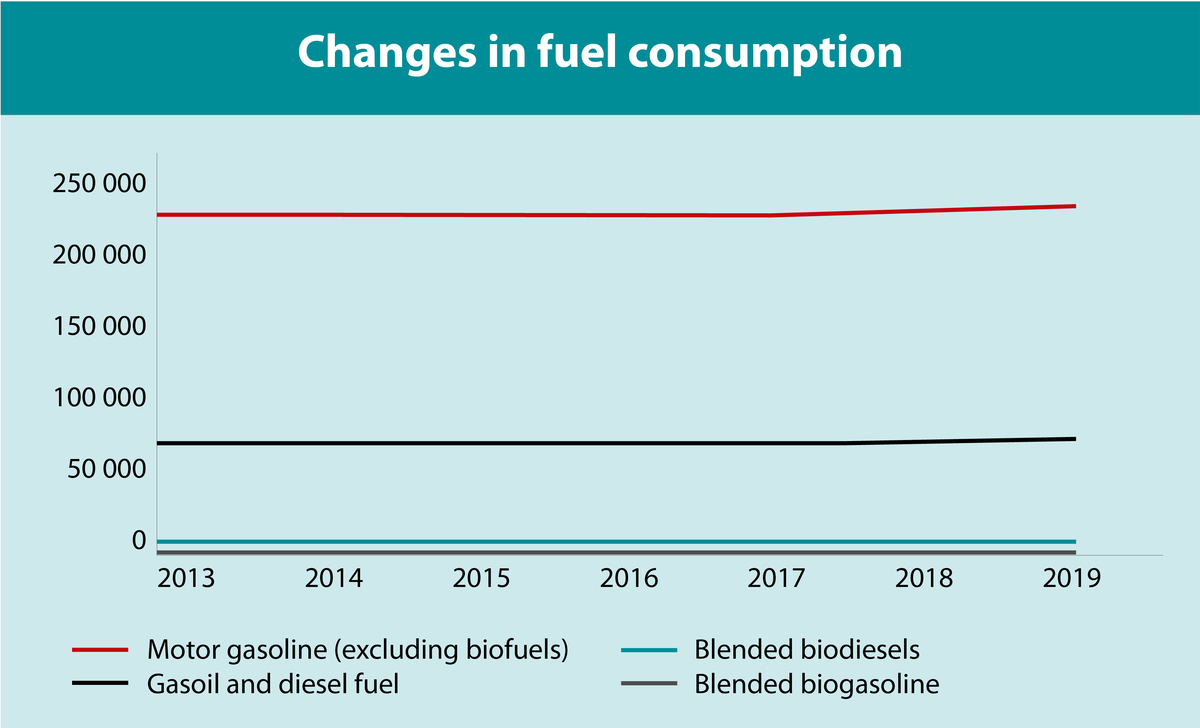

The European market (data for 4M 2020) has been performing in line with global trends. However, the experts have identified a number of features that are specific to Europe. For instance, despite falling demand for gasoil and motor gasolines, consumption of additives and oxygenates has increased, and blended gasolines (including biofuels) are growing.

Global seaborne shipments of motor fuels declined over six months by 11% year-on-year

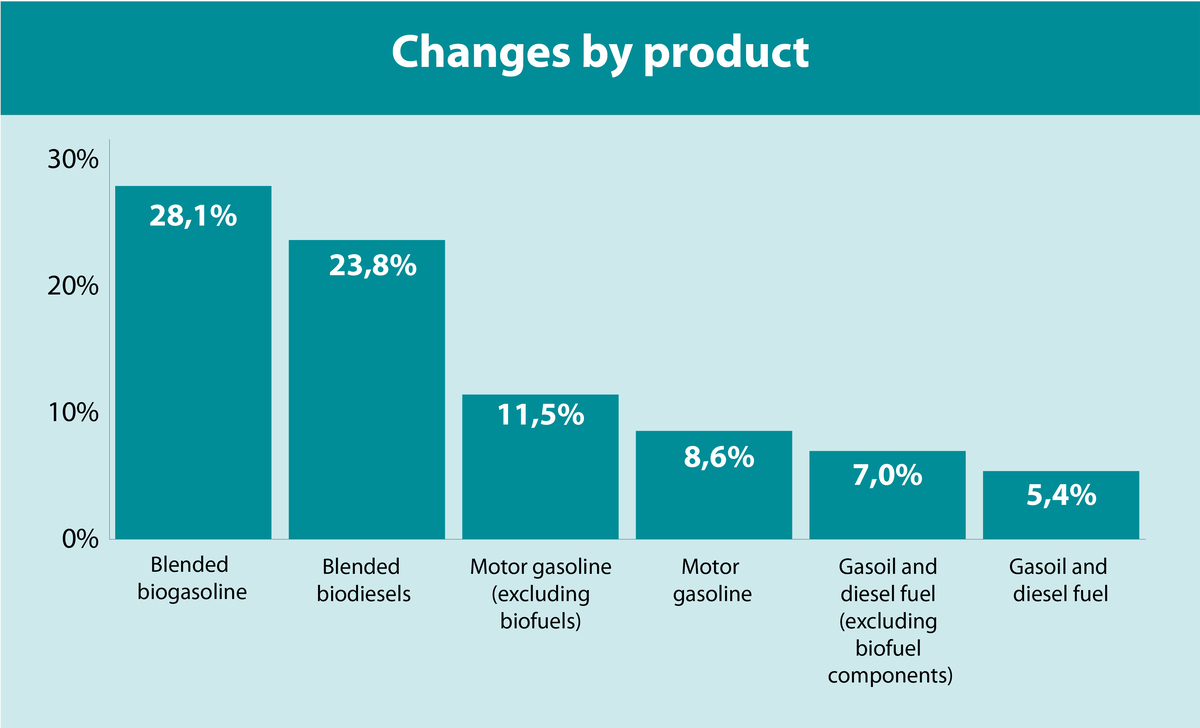

The biofuel consumption rates are increasing, and due to a low base this growth looks impressive

In order to understand what is happening in Europe besides the effects of COVID-19, we need to take a look at longer-term trends. For decades, the EU remained a “diesel” region, and this situation has not changed as far the overall vehicle fleet is concerned. However, the pressure on diesel-powered vehicles and investments into green technology has had an impact on the motor fuel market. Biofuel consumption rates are increasing, and due to a low base this growth looks impressive: +28.1% for blended biogasoline and 23.8% biodiesel (data for 4M 2020). Motor gasolines have been growing, while diesel sales have been falling, and for a number of years.

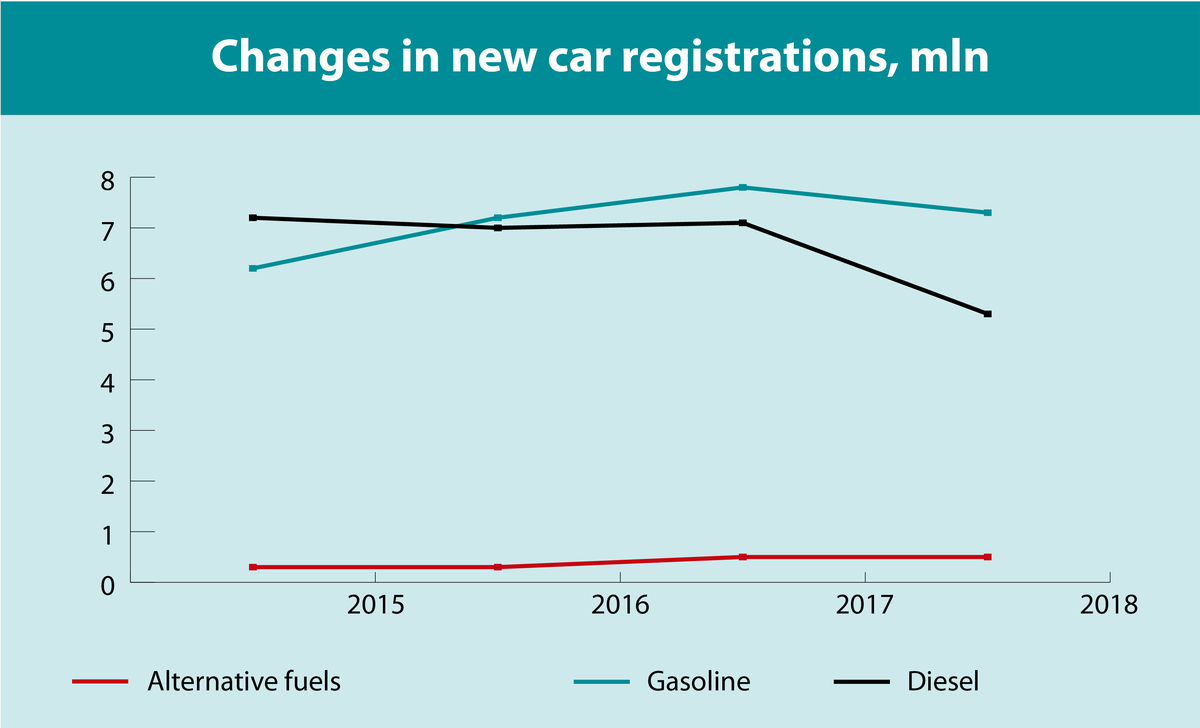

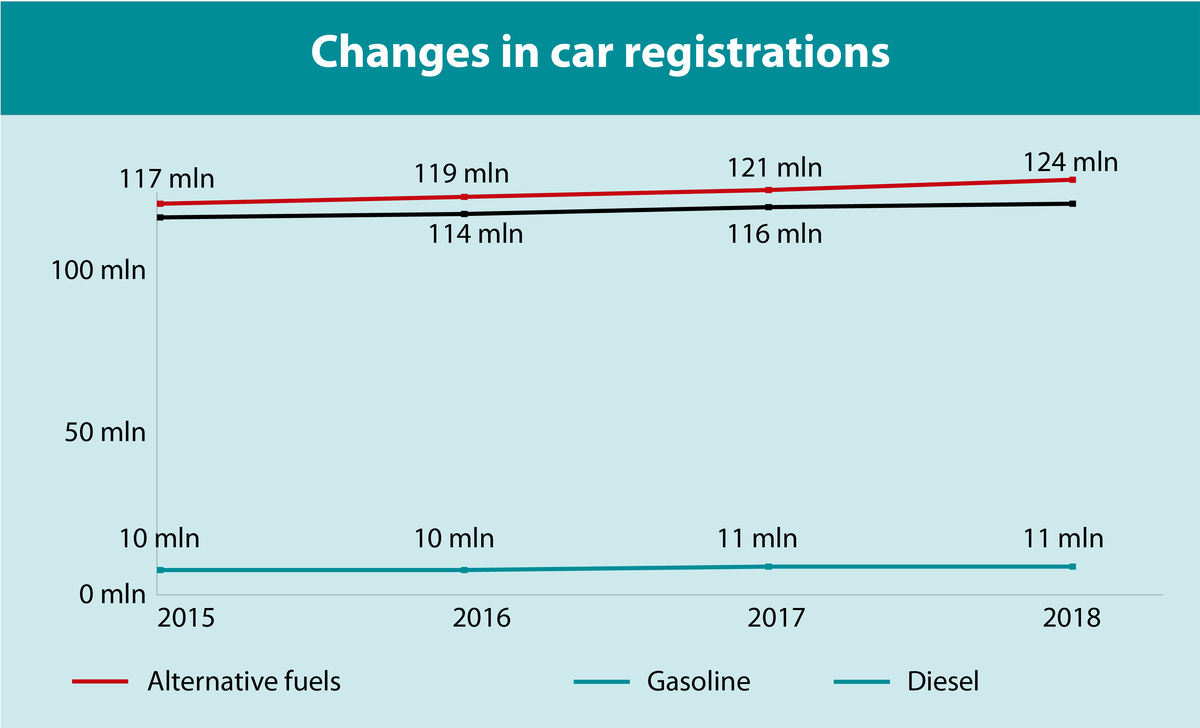

New car registration figures also may offer some interesting insights. Gasoline cars today lead the way, with annual sales of more than 6.3 million, compared to 4.1 million in 2018. The drop in diesel car sales from 6 to 4 million is a dramatic change that has occurred in virtually just a few years. The market has shifted toward gasoline rather than alternative fuels. Sales of cars running on alternative fuels, or electric cars, have also shown annual increases: in recent years, sales have grown from 100,000 to 500,000 vehicles per year. Percentage-wise, the growth has been impressive, but given Europe’s total vehicle fleet (273 million), the share of vehicles using renewable energy does not exceed 5%. This means that a rapid decline in the size of the traditional vehicle fleet is not to be expected – this process may take 10 to 20 years.

European motor fuel market structure (thousand tonnes)

Russia lags far behind Europe in terms of car ownership per 1,000 people. However, due to the specifics of the national economy, Russia is unlikely to close the gap to the EU countries

The widespread use of LPG as a motor fuel is another specific feature, although not in Western Europe. However, for example, liquefied petroleum gases account for more than 37% of motor fuels in Turkey, and demand for cars running on LPG is higher than for gasoline or diesel vehicles. We see a similar situation in Poland and a number of Balkan countries. “Such diversification cases, I believe, may be another reason why the transition to alternative fuels has been hampered. Still, the downward trend in the share of hydrocarbons is clear. As the vehicle fleet gets replaced, traditional fuel consumption will objectively decline while fuel efficiency requirements will increase, which is already driving demand for various additives,” says Alexander Shkulin.

Outlook for the Russian market

In Russia, according to Mr Shkulin, vehicle fleet growth in the coming decades will be limited by two factors – the country’s demographics and the structure of the national economy. The demographics metric, as estimated by Rosstat, will change only slightly: the growth or decline in the country’s population is capped at 3% by 2045–2050. Russia lags far behind Europe in terms of car ownership per 1,000 people. However, due to the specifics of the national economy, Russia is unlikely to close the gap to the EU countries. Russia’s economic growth traditionally relies on increases in oil prices and the subsequent rise in fuel prices. As consumers are becoming more cost-conscious, they are starting to switch to LPG, among others. Consumption shrinks in a contracting economy, and it would not be reasonable to expect increases in vehicle fleets. This means that the size of the motor fuel market will remain stable in the coming years. On the other hand, Russia’s vehicle fleet is relatively old, and its renewal is likely to be more dynamic than in other countries, leading to gradual declines in fuel consumption.

When assessing the Russian refining market, Mr Shkulin noted that a drop in oil production did not have any significant impact on the output of petroleum products. Against the backdrop of falling crude exports, producers have ramped up exports of diesel fuel, gasolines and other refined products, which has created an imbalance in the domestic market. For the first time, the government started imposing a windfall tax on industry players, with lockdowns creating distortions in demand for certain product groups. Combined, these factors have led to market uncertainty. Alexander Shkulin is convinced that “Against this background, we do not expect regulatory measures to be eased or the burden on the oil and gas industry to be reduced, rather the opposite.”

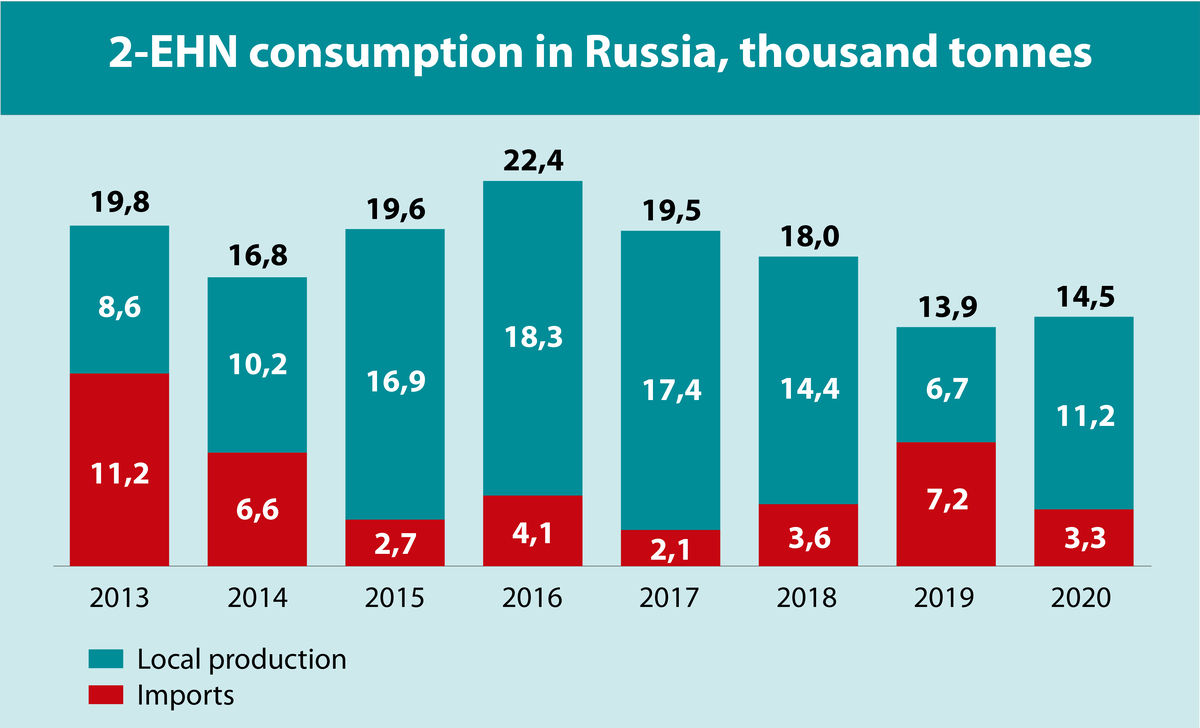

Consumption of additives has been declining across domestic operations due to refinery overhauls

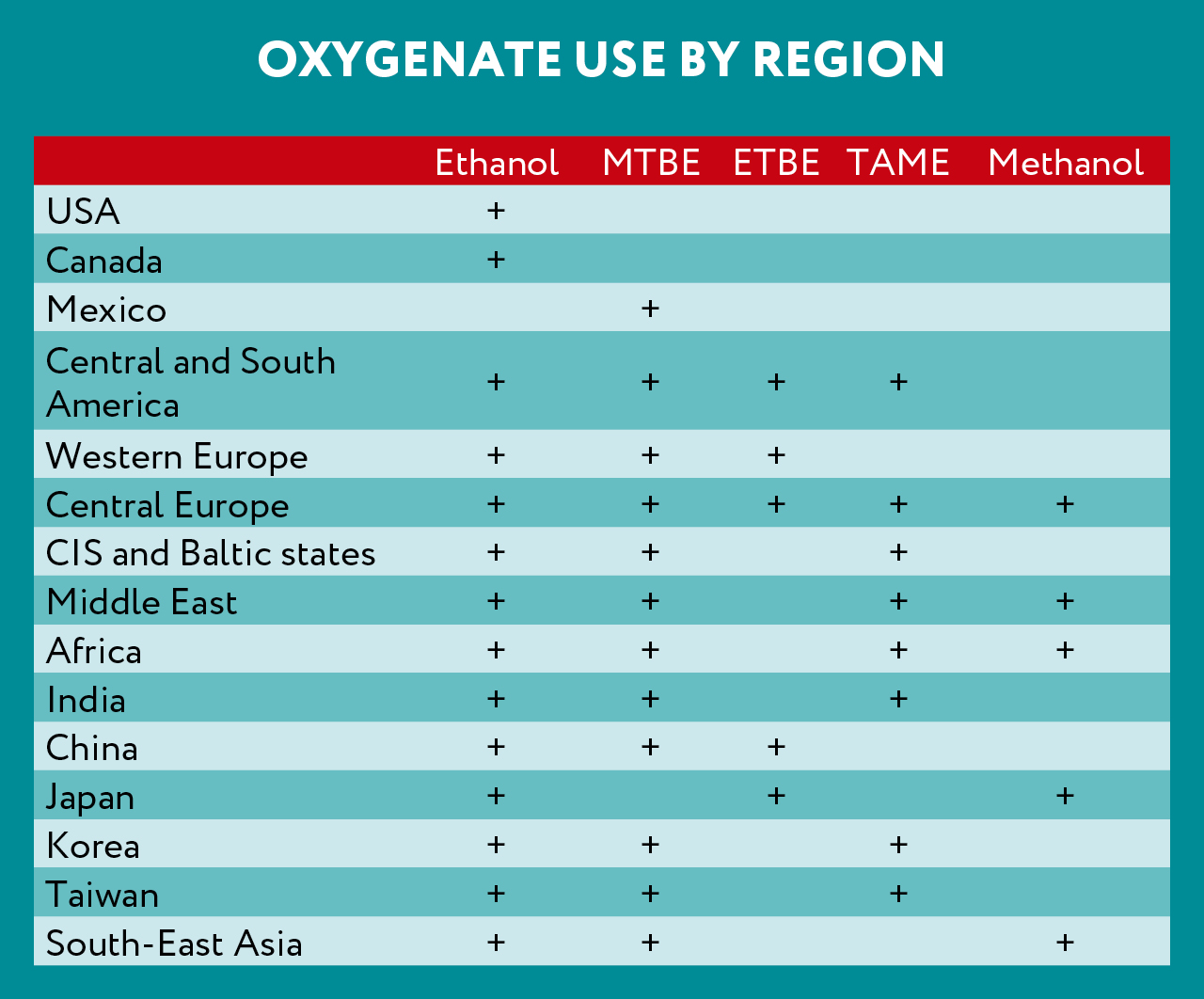

Anna Sysoyeva, an expert at SIBUR’s Plastics, Elastomers and Organic Synthesis Division, presented the participants with an overview of the market for fuel components and additives. She pointed out that SIBUR produces a number of octane enhancers, most notably methyl tertiary butyl ether (MTBE, used as an additive to motor fuels to raise the octane number of gasoline). Today, it is the second most widely used oxygenate globally. Ethanol is number one, used as a key fuel component in E85 fuel (in Brazil and Australia) and as a gasoline additive in Western Europe and the USA. MTBE has now reached maturity and is starting to feel the pressure from biofuel producers. Global MTBE demand is expected to decline by 0.5% p.a. in 2019–2025 due to surplus capacity. China’s decision (China accounts for over 45% of world MTBE consumption) to gradually switch to E10 gasoline and new capacity additions in the Middle East are reshaping the market landscape. The Eurasian Customs Union countries and Former Soviet Union (FSU) states will remain the key markets for domestic producers of oxygenates in the coming years. The market expects a gradual reduction in demand due to refinery overhauls and the refiners using their own oxygenates. Surplus capacity and weakening demand will push players to exit and reshape the market.

Similar dynamics are at play in the cetane improvers segment. According to Denis Gerber, a lead expert at SIBUR’s Plastics, Elastomers and Organic Synthesis Division, 2-ethylhexyl nitrate (2-EHN) is the most popular diesel fuel additive globally. In Russia, only two companies manufacture this additive and two more produce feedstocks for it, with SIBUR being the largest player. Consumption of this additive has been declining across domestic operations due to refinery overhauls. Demand in Europe has been on the one hand falling, due to lower diesel consumption, and on the other hand growing as regulators introduce higher fuel quality standards.

Establishing a special support regime for biofuels is hardly a good idea

One of the topics raised at the conference was biofuel’s prospects in Russia. Anatoly Keshitsky, a representative of Oduvanchik (a fuel additive producer), noted that no infrastructure or economic opportunities exist yet in Russia to introduce such products into the market. “We have considered both production and distribution technology for biodiesel and bioethanol. Despite the fact that the cost of producing a litre of biofuel in our region (Altai) is just 22 roubles, excise duties, taxes and government regulation are unlikely to make the marketing of this product viable. We can talk all we want about environmental protection, but at the end of the day, consumers will vote with their money. And unless the government introduces special support regimes for this type of fuel, we can’t think of an environment wh ere such a business would be attractive – all the more because there are a number of technological restrictions on fuel sales at Russia’s filling stations.”

Other panellists generally agreed with this assessment, noting that establishing a special support regime for biofuels is hardly a good idea. The next step would be for alternative fuels to start squeezing out gasolines and diesel fuel, which would lead to the need to either cut refining capacity or introduce special support measures – this time to bolster refiners.

The presentations were followed by a discussion, wh ere video conference participants shared their views on the current market situation. Denis Demin, Head of Strategic Analysis at Gazprom Neft, pointed out that despite the apocalyptic forecasts made in spring, when markets were expected to fall by 25% to 30%, current statistics suggest a 17% to 20% drop. “On the one hand, it’s not that scary, but on the other, the outlook for recovery in demand seems to be less ‘exciting’. Indeed, we have seen a rebound; however, by the end of the year this curve will gradually flatten out, with hydrocarbon consumption for the full year down 3% to 5% from 2019. The ultimate recovery will take place at the turn of 2021–2022,” he stressed.

One of the reasons is overproduction for a number of products. A regular refinery does not have the required flexibility to adjust the production of specific products. This is why, for example, a number of companies in Europe have had a hard time selling products for which demand has fallen sharply. The supply glut that has built up at the time is still weighing on the market and hindering the recovery of prices and production volumes. This is particularly noticeable when looking at prices that offer low margins, even despite a higher demand for petroleum products. With revenues falling and the social burden on businesses (pandemic-related restrictions on staff reductions imposed by a slew of governments) increasing, some owners have already voiced their concerns, asking: “Do we really need these kinds of assets?”

Refining in the Old World has long been under strong competitive pressure, and when a crisis strikes, competition intensifies

“This is not a new situation for Europe. Refining in the Old World has long been under strong competitive pressure, and when a crisis strikes, competition intensifies. Clearly, the problem will ease after spreads ultimately recover; however, we are yet to turn a page on refining capacity rationalisation. Excess capacity is something that will haunt the sector until some sort of balance is found,” claims Denis Demin.

Another point he made was that a number of experts underestimate Europe’s “passion” for green technology. In his opinion, it is actually decarbonisation investments that are currently being trumpeted by EU officials as an engine of growth for the eurozone. This means that the dynamics of the vehicle fleet and of the entire motor fuel market may start to change more radically as early as in the medium term.

“Since making forecasts today has become an almost futile exercise, we at the Company have made it a rule to consider several scenarios and see crisis as a chance for new opportunities above all. Our team’s current motto is two words: ‘speed’ and ‘agility’. These qualities, I believe, are the most useful ones for business and enable us to come up sometimes with unconventional, breakthrough solutions.”

Download PDF