By making these forays, oil companies seek to increase the monetisation of their raw material output through the production of polymers and other chemicals. The arrival of new players, however, will put pressure on industry margins and increase competition in the domestic market.

Low oil prices, OPEC+ production cuts and reduced demand for raw materials and fuel due to the COVID-19 pandemic have driven home the need for oil and gas companies to diversify their business. In this context, the Russian plastics sector, growing steadily at 7% per year, looks attractive, and the monetisation of hydrocarbons through the production of polymers and other petrochemicals seems to hold great promise. Key players in the oil and gas sector already have significant chemical capacities integrated into their operations. Last year, LUKOIL produced 1.1 million tonnes of petrochemical products at its Saratovorgsintez, Stavrolen, LUKOIL Neftochim Burgas and ISAB S.r.l. plants. Novokuibyshevsk Petrochemical Company, Angarsk Polymer Plant and Ufaorgsintez (with a total output of over 2.1 million tonnes of petrochemicals in 2019) are part of Rosneft. TAIF is also a major producer of synthetic rubbers and plastics (key facilities being Nizhnekamskneftekhim and Kazanorgsintez).

The Russian plastics sector, growing steadily at 7% per year, looks attractive

Nina Adamova, Senior Analyst at Gazprombank’s Centre for Economic Forecasting, notes that subsidiaries of major diversified oil and gas companies account for about 27% of Russia’s ethylene capacity mix, adding that “typically, however, chemicals are not a core business for large diversified commodity producers.” Previously, investments in these operations were made mainly for asset maintenance, not asset expansion. The situation has changed as competition increased in a volatile hydrocarbon price environment. Diversified companies saw the petrochemicals sector as an opportunity to diversify their business and make it more resilient in a volatile hydrocarbons market, i.e. they found an alternative way of monetising these resources. “This is why recently we have seen increasingly frequent announcements by oil and gas companies to focus not only on brownfield development but also on greenfield projects in the petrochemicals sector,” she says. However, according to Nina Adamova, these projects often have a fairly simple configuration and do not involve deep conversion, or are designed to integrate new units into existing integrated operations.

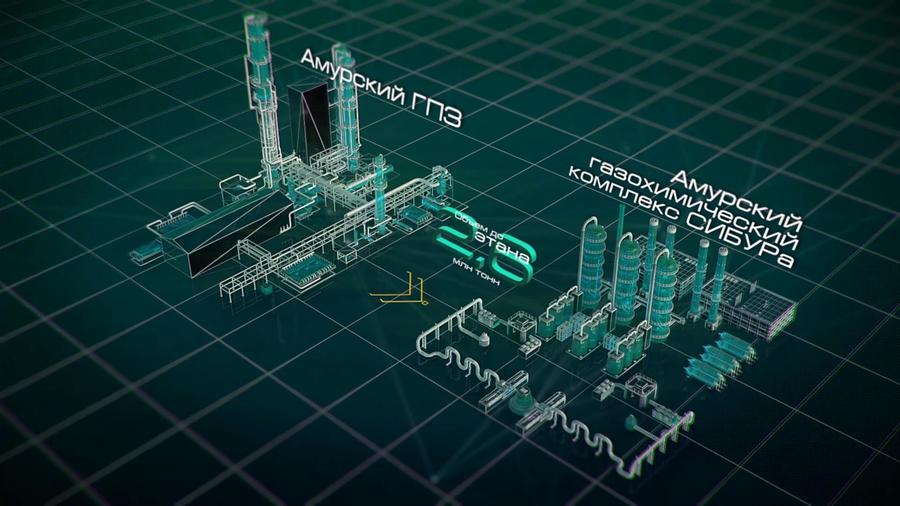

Visualisation of petrochemical cluster projects in the Amur Region: Amur GPP (Gazprom), Amur GCC (SIBUR).

She is echoed by Dmitry Akishin fr om VYGON Consulting. According to him, refinery-petrochemical integration is not a new trend in Russia, and there are many refinery complexes producing petrochemical products as well (in Tatarstan, Bashkortostan, the Stavropol Territory and other regions). “Global oil and gas majors such as BP, Shell and Total have always had their own petrochemicals divisions,” he points out, adding that “at the same time, despite the fact that EBITDA margins offered by petrochemicals can exceed 40% vs 5% to 7% for refineries, oil and gas companies did not rush to place bets on petrochemicals.” Firstly, petrochemicals are much more investment intensive than refining operations. “In addition, a focus on such a complex business often requires a separate business to be set up within their vertically integrated oil organisation,” he explains. Nevertheless, in the past 5 to 7 years, the trend for oil companies to tap into the petrochemicals market has increased significantly. “There are virtually no new major refinery projects now that do not produce petrochemical products too. Some of them will focus on crude oil-to-chemicals (COTC) technology, where the volume of petrochemicals can reach 50% to 60% of total refinery output,” says Mr Akishin.

Diversified companies saw the petrochemicals sector as an opportunity to diversify their business and make it more resilient in a volatile hydrocarbons market

At the same time, oil and gas companies have a number of competitive advantages over incumbents. Some types of petrochemical products (propylene, benzene, etc.) are produced as refinery by-products, so their processing can enable the production of higher-value products through deeper conversion at relatively low cost. For example, Gazprom Neft and SIBUR launched polypropylene production at Gazprom Neft’s Moscow Refinery. “We should also keep in mind the financial strength of oil companies,” says Mr Akishin. “Their CAPEX programmes have historically dwarfed those of petchem players.”

Alternative energy – a driver reinventing the business of global majors.

New players coming into the petrochemicals market

The Russian Government is keen to promote the expansion of the domestic petrochemicals sector. As noted in the 2025 industry road map, approved by the Government in March 2019, the Russian petrochemicals sector has a strategic importance to the national economy. According to estimates by the Cabinet of Ministers, the top 8 largest petrochemicals projects can add more than 8 million tonnes of new polyethylene and propylene capacity (2.3 times the current level), bringing total production of bulk polymers from 5.3 million tonnes in 2019 to 11.1 million tonnes by 2025 and ramping up exports from 600,000 tonnes in 2020 to 4.4 million tonnes by 2025. In late September, Deputy Prime Minister Yury Borisov, who oversees the fuel and energy sector, voiced even more ambitious plans: in his view, Russia is capable of growing its plastics production by 10 to 15 million tonnes, thereby capturing about 15% of incremental global demand. The Ministry of Energy expects the overall global chemicals market to double by 2030 from the current USD 4.5 trillion. However, as new players are entering the sector in increasing numbers and with new capacity additions continuously growing in size, competition in the market is set to become more intense.

SIBUR is currently the leader in the Russian petrochemicals market. In late 2019, SIBUR launched ZapSibNeftekhim, Russia’s largest petrochemical facility, with a capacity of about 500 ktpa of propylene, 100 ktpa of butane-butylene fraction and 1.5 mtpa of various polyethylene grades. The project will fully cover the needs of the domestic market for polyethylene, which has been in short supply so far, and will export volumes that are not consumed locally.

The Ministry of Energy expects the global chemicals market to double by 2030 from the current USD 4.5 trillion

The Company has also launched the construction of an even more ambitious project in Russia’s Far East – the Amur Gas Chemical Complex, which will comprise the world’s largest steam cracker, as well as facilities to produce 2.3 million tonnes of polyethylene and 400,000 tonnes of polypropylene, mostly for export into Asian markets. Construction is not expected to be completed before 2024.

However, by that time the Russian chemicals market may already have a few new entrants – oil and gas companies whose projects are considered in the industry roadmap. These include RusKhimAlliance (a joint venture between Gazprom and Artem Obolensky’s RusGazDobycha), established to build a USD 20 billion complex in Ust-Luga, which will process 45 bcm of gas to produce 13 mtpa of liquefied natural gas (LNG), up to 4 mtpa of ethane and over 2.2 mtpa of liquefied petroleum gas (LPG). Ethane will be used as a feedstock to produce 3 mtpa of various polyethylene grades.

Around 500 ktpa of polypropylene will be produced in the near future by LUKOIL at its Nizhegorodnefteorgsintez Refinery in Kstovo, Nizhny Novgorod Region. LUKOIL explains that the refinery’s PP unit could well become Russia’s largest petrochemical facility that is integrated with refining processes within a single production site. LUKOIL says that the domestic market is a priority destination for its products; however, details of future supplies will be finalised depending on the market conditions. The company is preparing to launch another major polypropylene and polyethylene project at its Stavrolen site in Budennovsk (Stavropol Territory) after 2024. The approximately USD 2 billion project will process 1 bcm of gas per annum, fed from LUKOIL’s Caspian fields. LUKOIL is expected to take a final investment decision on the project before the end of 2020. Overall, the company’s petrochemicals strategy, which it has never publicly unveiled, has included at least two other major polymer projects.

LUKOIL-Nizhegorodnefteorgsintez Refinery.

Irkutsk Oil Company plans to invest a similar amount in its 650 ktpa polyethylene project in Ust-Kut, Irkutsk Region, by 2024. Tatneft has also announced ambitious petrochemical expansion plans: the company intends to build a complex in Tatarstan with a phase one design capacity of approximately 250 ktpa of polypropylene. The configuration of phase two is yet to be finalised, but will include an ethylene complex and the development of polyethylene, plastics and polystyrene clusters.

TAIF also plans new capacity additions for polypropylene and other plastics. The company intends to build a new 1.2 mtpa ethylene complex at the Nizhnekamskneftekhim site, which will triple its ethylene capacity to 1.8 million tonnes and ramp up plastics output to 2.5 million tonnes. Phase one is expected to come on stream in 2023, with polymer production start-up three to four months before the launch of its Ethylene-600 plant. The company then expects to launch the construction of phase two, slated for completion in 2027.

Additional tax breaks are being considered for Rosneft, which had plans to build a major petrochemical plant in the Primorye Territory – the Eastern Petrochemical Company (VNKhK) complex. Phase one of the project envisaged a 12 mtpa refining capacity, with phase two adding a 3.4 mtpa petrochemical capacity. In 2019, the company announced a freeze on its project, saying it was economically unviable in the context of the Russian oil industry’s “tax manoeuvre”. However, in late September, the Government asked Rosneft to provide an additional business case based on a cost/benefit analysis of the project in a government support scenario. Still, specific tax benefits for the project have not been approved yet, and its implementation remains open to question. The Ministry of Energy now expects the petrochemical phase of VNKhK to come online in 2026 and the refinery to come on stream by 2029.

Oil companies’ entry into the petrochemicals sector will have a significant impact, particularly given the scale of the announced projects

However, experts point out that the petrochemicals sector has its own pitfalls. “On average, gross margins in the industry over recent years have been 5 to 7 percentage points higher than in oil refining; however, the amount of revenue flows in the refining industry is an order of magnitude higher – by 15 to 16 times,” says Nina Adamova. “The chemical business is complicated due to the specifics of its technology, fragmented market for its products, the need for targeted but smart and timely capital investments and other aspects that make it difficult for new players to enter the sector,” Ms Adamova explains.

In her opinion, if the projects announced by these oil and gas companies are successfully implemented, Russia’s petrochemical capacity might increase by more than 1.5 times in the next five years or so, which will both boost exports of basic polymers from Russia and drive the development of local polymer processing.

A condensate processing unit at Nizhnekamskneftekhim.

A global change

Analysts agree that oil companies’ entry into the petrochemicals sector will have a significant impact, particularly given the scale of the announced projects. Dmitry Akishin points out that the capacity of modern refineries is incomparable to classical petrochemical operations. This is particularly noticeable in Asian markets, with their production and demand largely driving the global chemicals sector. For example, Hengli’s 20 mtpa COTC complex, already commissioned in China, can produce over 4 mtpa of paraxylene (a feedstock for polystyrene and plastics), while Zhejiang’s planned complex has a total design capacity of 40 mtpa of crude and will also produce about 8 mtpa of paraxylene.

Ms Adamova notes that new capacity additions and reduced reliance on imports in Asia-Pacific and China in particular will be the biggest drivers for the global market balance in the medium term. The big question is which quartile of the cost curve these new plants will stand in. In her view, Russian players are likely to have the most advantageous positions.

However, capturing global demand does not preclude competition. Given the scale of new capacity additions, small producers will have to move away from bulk chemicals and shift to specialties.

Worried about the prospects of increased competition in Russia, certain producers are already asking the Government to close off the domestic market at least to external suppliers. For instance, in late September, the Council of the Eurasian Economic Commission (EEC) raised the import duty for one year on certain types of LDPE to the maximum rate permitted by the WTO (6.5%), a measure requested by Kazanorgsintez. The EEC claims that TAIF and SIBUR, manufacturers of these products, are able to meet the needs not only of the Russian market but also of the entire Eurasian Economic Union.

Not all the projects announced by Russian oil and gas companies will be implemented

Green energy is another trend affecting oil and gas companies. International majors such as ExxonMobil, Chevron, ConocoPhillips, BP, Shell, Total, Eni and Equinor intend to review their energy policies in the near future and divest a total of up to 68 Bboe of resource assets in various geographies for an estimated USD 111 billion. They plan to use the proceeds to expand their respective renewables, hydrogen and electricity portfolios. As of 2018, these companies allocated on average 3% to 5% of total investments to renewables and related projects within the energy transition strategy, which aims to make the European Union the world’s first climate-neutral continent by 2050. Already now, the share of renewables in Europe’s power generation has hit a record 35%.

Hengli Petrochemical Refining Co., Ltd. (Dalian, northeast China).

At the same time, the coronavirus pandemic may accelerate the process of oil and gas companies boosting their renewable energy capacity. The Ministry of Energy states that while initially the share of hydrocarbon energy was expected to decrease from approximately 85% to 75% by 2040, now the forecasts are being downgraded – an opinion supported by International Energy Agency (IEA) estimates. The IEA points out that pandemic-related restrictive measures have led to a marked increase in the use of low-carbon alternatives, which can bring their share of power generation to as much as 40%.

Dmitry Akishin explains that the green trend is definitely impacting the structure of the petrochemicals industry. An EU carbon border tax, currently under development, indirectly stimulates deeper hydrocarbon conversion. Many financial institutions are reluctant to finance projects related to classical hydrocarbon processing. However, he expects deeper integration between refining and petrochemicals.

This trend will be particularly relevant for Russia, wh ere scepticism about the transition to renewables still runs high. On the other hand, many in the market are confident that not all the projects announced by Russian oil and gas companies will be implemented. Much will depend on market conditions, but a transformation of this magnitude will create excessive competition among domestic players and will affect the petrochemicals industry as a whole.

Download PDF