TO THE READER

by Pavel Lyakhovich, member of the Management Board and Managing Director of SIBUR.

Cold season

Waiting for summer with its traditionally high sales of soft drinks, outdoor picnic cookware and garden tools proved to be in vain for companies that manufacture packaging and other products. It was the abnormal weather that upset the apple cart.

Filling the shortage

In 2019, SIBUR will launch the DOTP investment project.

“Green” packaging

SIBUR presented its products at Interpack (Germany) and RosUpack (Russia).

Fundamental gas

SIBUR upgrades Yuzhno-Balyksky GPP.

Bridging the gap

All the necessary information is now available for our Clients in a dedicated section of SIBUR's website.

A valuable practice

BIAXPLEN expands its customer communication channels to include technical workshops and webinars.

Stronger together

SIBUR and TechnoNICOL discussed key cooperation themes.

Choosing the right colour

SIBUR’s Togliatti site introduces new packaging labels.

Favourable location

SIBUR will set up a logistics hub for polymer products in the Kaluga Region.

NPP Neftekhimiya: among the best

Basell Poliolefine Italia has included the joint venture of SIBUR and Gazprom Neft in its Top-10 ranking.

Never stop learning

SIBUR becomes partner of a professional development course at the Russian University of Transport (MIIT).

Along the Silk Way

SIBUR acted as Silk Way Rally's technical partner for innovative materials.

Brand Guide

SIBUR: corporate logo use.

Private Public

Some companies came up with rules and recommendations about social networks for their employees.

I saw, I understood, I integrated

Digital business transformation acts as a catalyst of change in the chemicals market.

Universal soldier

Thermoplastic elastomers were the key topic of the customer conference held by SIBUR.

Landfill impossible recycle

From 2019, an extensive list of plastic waste will be prohibited from being buried in landfill sites.

New opportunities in the online universe

E-commerce opens up brand new opportunities for manufacturers of polymer packaging.

Face to face

How to put out a magnesium fire, manage waste and make polymers fight bacteria – those were the ideas suggested by the IQ-CHem contest participants.

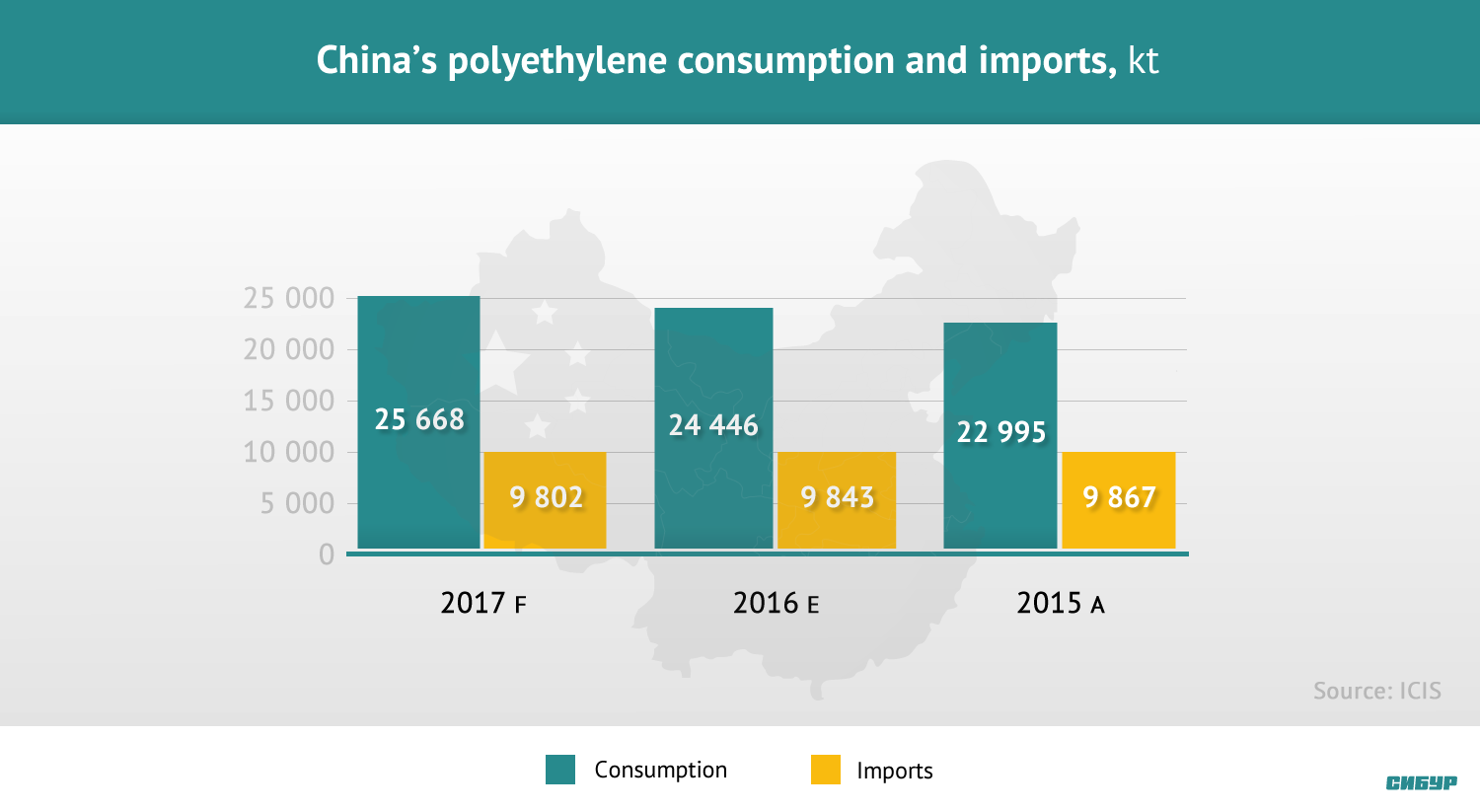

Sights set on China

Asia to become a major polyethylene consumer.

Ten colours for multi-layer films

Igor Esin, CEO at TIKO-Plastic, dwells on what consumers expect from flexible polymer packaging and what can be done to satisfy them.

We can learn a lot from each other

Meet Wenzhi Zou, a new member of SIBUR’s Management Board.

TOP MANAGERS TAKING QUESTIONS

In the Q&As section, our top managers answer the most interesting and relevant questions from our clients sent to dearcustomer@sibur.ru.