TO THE READER

Dmitry Konov, Chairman of the Management Board at SIBUR Holding, takes a focus on SIBUR’s past, present and future, its key business milestones and new opportunities for Clients.

SIBUR: from 1995 to the latest developments

In this 10th anniversary issue of our magazine, we looked back at SIBUR’s key milestones and talked to clients that have been directly involved.

Journey towards digital business

Dmitry Konov, Chairman of the Management Board at SIBUR Holding, spoke at the Open Innovations Forum.

Green light to sustainability

How to minimise the environmental footprint with air pollution control equipment.

Client Editorial Board

SIBUR for Clients welcomes its readers to the Client Editorial Board.

Development trends

SIBUR’s fourth customer conference on SBS polymers took place in Nizhny Novgorod.

A focus towards creativity

BIAXPLEN’s round table talk has attracted over 100 participants.

Hailing innovation

In October, Vienna became the venue for EPCA 52nd Annual Meeting gathering chemical majors.

Shape tomorrow

For the first time, SIBUR has taken part in SHAPE TOMORROW, the European Innovation Summit in Frankfurt, Germany.

FAKUMA 2018

SIBUR presented the full range of polyolefins to be produced by ZapSibNeftekhim at international trade fair for plastics processing.

Paints and varnishes – in search of solutions

Paints and varnishes market players gathered at the annual conference in Sochi to discuss this year's performance and future prospects.

Road 2018

Representatives of the government, industry associations and the business community gathered at the Road 2018 exhibition to discuss the challenges of the road construction industry.

Polystyrene: gaining traction

SIBUR experts are optimistic about prospects of the Russian polystyrene market.

Forbes 200

SIBUR came in 13th in Forbes' ranking of Russia’s Top 200 private companies.

Film Festival Grand Prix

A film by SIBUR won the US International Film & Video Festival award.

Eco-friendly solution

SIBUR set to sort consumer plastic and paper waste at its Tomsk site.

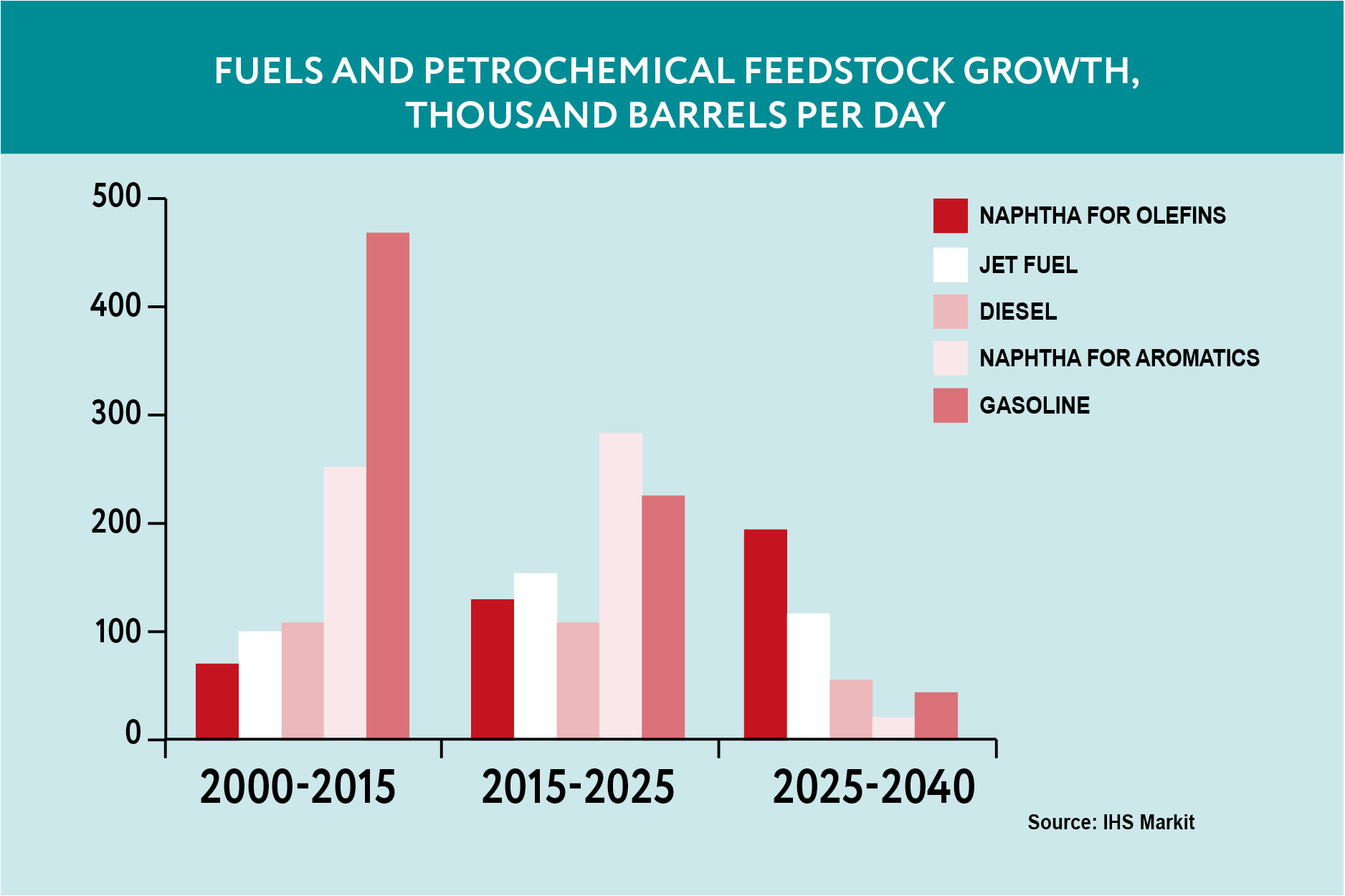

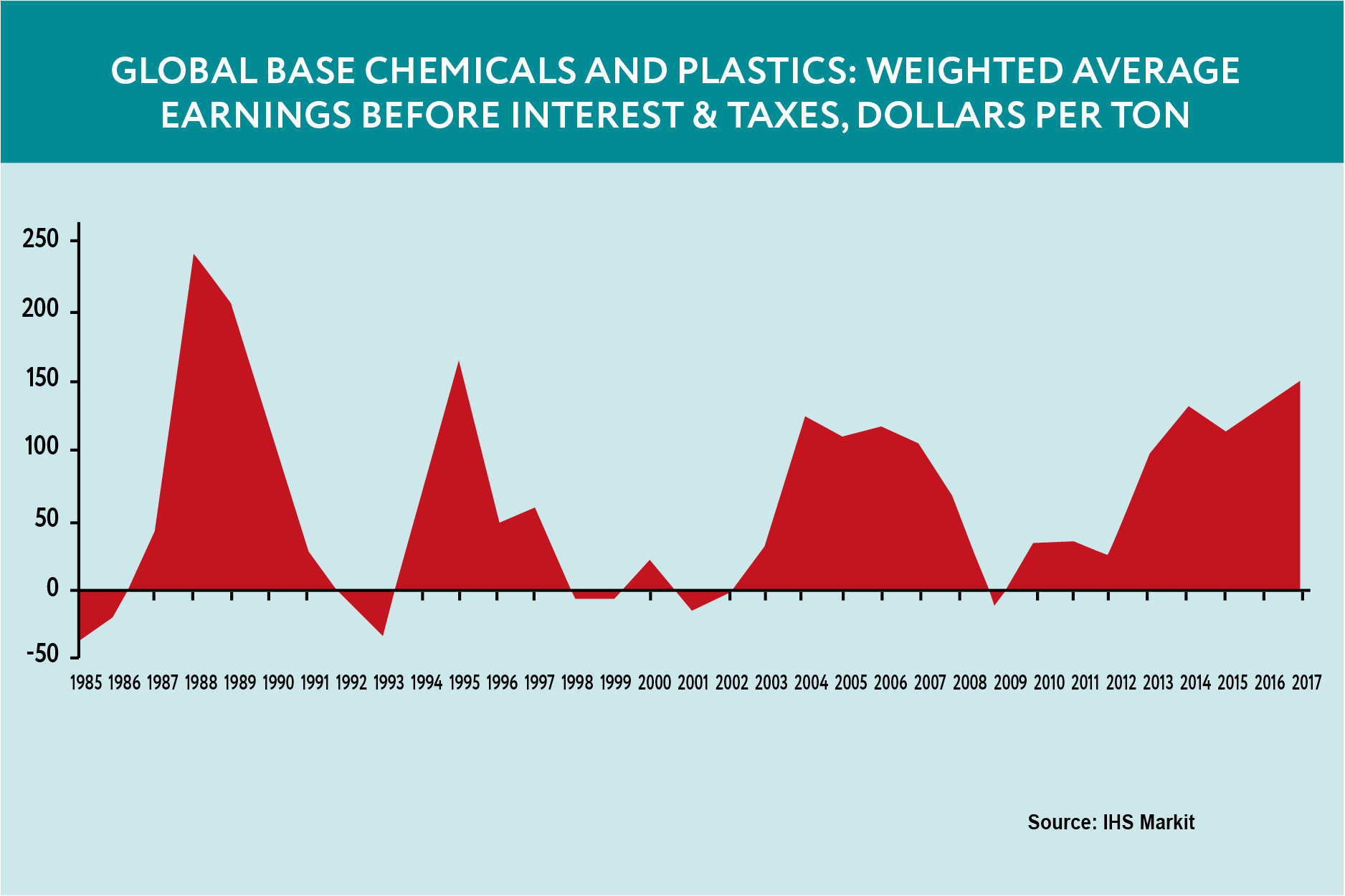

The golden age

Roger Green, Vice President for Chemical Consulting at IHS Markit: "The petrochemical industry is in golden age now".

Chinese market: growth potential

Today, China is one of the most attractive markets for Russia.

2018/2019 winter trends

Seasonal overview of the winter tyre and automotive chemicals market

BOPP films – flexible strategy

Domestic players at the BOPP film market are committed to ensuring full imports substitution.

What threatens the growing ethylene market?

The ethylene market growth is driven by consumer demand for everyday products.

SBS polymers: high potential

The additional capacity of SIBUR’s Voronezh site will enable the Company to roll out new products.

Clusters as pockets of growth

Participants of the Russian Energy Week have discussed challenges of industry clustering.

Dr Sergey Alekseenko:

“The world is rapidly transitioning to alternative sources of energy”.

Unwasted opportunity

Most exciting ways to collect and recycle waste.

Evolution of recycling

How waste affects economy.

Industry as a single interconnected organism

Roman Kizimov, CEO of TD Plastic, speaks about his company's key development areas and marketing techniques.

Rolling with the punches

SIBUR’s CEO Mikhail Karisalov on avoiding burnout and making sports part of daily life.

Key value

SIBUR conducts its 3rd Focus on Customer Contest: application period ended on 23 November, with winners to be announced by the end of the year.

Five rules of a true leader

Ann Cairns, vice chairman of Mastercard, offers an unorthodox view of leadership values.

TOP MANAGERS TAKING QUESTIONS

In the Q&As section, our top managers answer the most interesting and relevant questions from our clients sent to dearcustomer@sibur.ru.

Roger Green

Vice President with IHS Markit, based in London. Roger leads the Europe & Africa Roger has delivered an extensive range of consulting engagements during a career of more than 25 years in the chemicals industry. He leads a team that works with clients on investment-related projects, mergers and acquisitions, market studies, project financing, and technology assessments.