Import substitution is the key driver supporting the demand for the entire range of domestically produced auto chemicals. Our market summary outlines the key trends of outgoing year in the segments of antifreezes, car screen washes and winter tyres.

Seasonality is a common driver of the automotive chemicals market, and, according to the experts, 2018 was no exception, with autumn months having enjoyed the peak demand and price levels.

A notable trend of 2018 is the mass production of private label auto chemicals by retail and gas station networks.

“Major manufacturers of auto chemicals were making winter preparations all through the year, purchasing raw materials and accumulating warehouse stocks ahead of the winter season,” said Alexander Sergeev, Head of the Union of Consumers and Manufacturers of Car Care Products. “Unlike them, smaller companies planned their procurement needs based on demand.”

According to Gennady Cherevko, Deputy CCO at Gelena Chemauto, a car chemicals maker, in late 2018, demand has gradually shifted fr om the premium to medium price segment, moving swiftly further down towards the economy brands.

The low-price category has been spearheading the late 2018 trend, which involved the mass launch of auto chemical private labels by retail and gas station networks. While helping market players to boost their brand awareness, this turn has also tightened competition in the low-price segment bringing benefits to both sellers and buyers.

With targeted import substitution among the factors supporting this trend, Gennady Cherevko relies on “substitution of imported components with high-quality Russian products” to drive the cost of production and the cost of end products further down.

Retail and gas station networks aggressively engage in production of auto chemicals under their own brands.

The compulsory admission of foreign bids to competitive procurement of goods and services by Russian public sector entities (pursuant to Federal Law No. 44-FZ) stands in the way of bona fide players looking to win the domestic market.

It’s all about climate zones

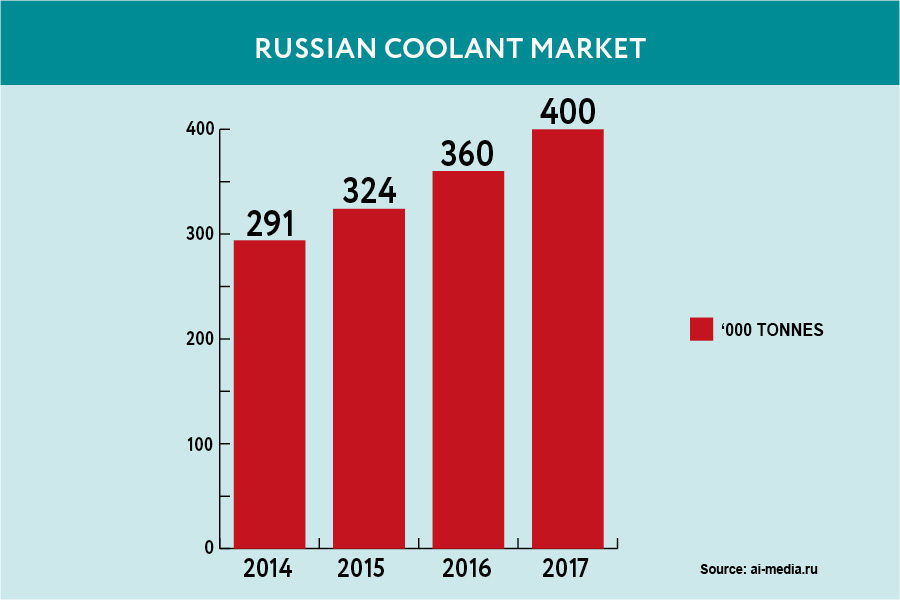

According to expert estimates, late 2018 has seen a slight increase in antifreeze sales, with large cities accounting for over a half (57–58%) of total sales.

Late 2018 has seen a slight increase in antifreeze sales, with large cities accounting for over a half (57–58%) of total sales.

Antifreezes enjoy the highest demand, while the demand for cooling liquids is significantly lower. “This is due to the greater share of foreign-built cars in the Russian market, as cooling liquids are mostly used for domestic cars,” explains Alexander Sergeev. Experts warn against cheap and increasingly popular cooling mixtures based on harmful methanol rather than diethylene glycol used in original coolant formulations. As the quality of raw materials is critical to the quality and service life of antifreezes, the desire to save often backfires.

According to Vladimir Zorin, CEO of an auto parts store, owners of domestically produced cars mostly prefer red Nord antifreeze, while owners of foreign cars buy various brands of blue J11 and J12 antifreezes. Purple J13 antifreeze is also gaining traction, offering a five-year service life and coming with a fluorescent additive, which enables easier identification of leaks and their sources in the darkness.

Foreign car owners prefer various brands of blue J11 and J12 antifreezes.

The demand for concentrated coolants that need to be mixed with water does not depend on climate and decreases every year, with these products now capturing about 4–5% of total sales.

“Each year, we see growing demand for 4 and 5 litre packs as opposed to the 10 litre ones,” says Alexander Sergeev. This trend is not only relevant for antifreezes, but also for winter screen washes. The cost savings coming with a 10-litre pack are not that big and the smaller pack is much easier to pour into the tank. Besides, the smaller pack needs less boot space and lasts long enough in cars that drive moderate distances (e. g. for non-daily trips around the city). The pattern of demand for winter screen washes varies depending on the climate zone. In Siberia and the Russian Far East, consumers prefer products suitable for lower temperatures, with prices increasing in line with the geographical remoteness of a region.

Winter car washes with a freezing point of under -30oC are mostly popular in Central Russia. Vladimir Zorin notes high demand for brands such as Nord Stream (-25°C), Spectrol Lemon (-30°C) and Liqui Moly (-25°C).

In the southern regions, wh ere there is almost never any frost, drivers opt for washes with a higher pour point, including the cheaper and unsafe products. Despite this, the share of counterfeit screen washes, as in the case of cooling liquids, has been on a steady decline.

In Siberia and the Russian Far East, consumers prefer winter screen washes suitable for lower temperatures.

By the end of 2017, the Russian tyre market was estimated at about RUB 190 bn, accounting for some 12% of the total auto parts market.

First, counterfeit products which are supposed to withstand temperatures of -30°C or even -40°C often freeze as soon as the thermometer reaches -10°C or -15°C, while the original winter screen washes only get thicker without actually freezing.

Secondly, many cheap antifreezes and winter screen washes contain methanol releasing vapours associated with health risks. Each year sees further regulatory cuts to the permitted methanol content, driving up the cost of cheaper auto chemicals and leaving the cost of zero-methanol premium products unaffected.

In the meantime, the demand for coolant concentrates that need to be mixed with water does not depend on climate and decreases every year, with these products now capturing about 4–5% of total sales.

The auto chemicals market will continue skewing towards a greater share of domestic high-quality coolants with a further drop in demand for unsafe products associated with risks that do not offset cost benefits, experts say.

The rigours of winter driving

By the end of 2017, the Russian tyre market was estimated at about RUB 190 bn, accounting for some 12% of the total auto parts market. In 2017, tyre sales increased by 20% as compared to 2016, with even more impressive growth expected by the end of 2018.

Tyre sales closely correlate with the sales of new cars, as they always go with summer tyres only. Hence, growth in the car market drives the demand for winter tyres. In 2016, for instance, the Russian car market grew by 11%. Experts estimate that domestic producers account for circa 60% of the Russian tyre market.

Tyre service centres account for more than a third of tyre sales.

Much like the auto chemicals market, the tyre market is seeing a shift in demand towards cheaper products. “Still, drivers are far from trying to save on safety and change tyres in due time,” says Alexander Eremin, representative of Cordiant, a tyre-making company. “Some 70% of winter tyres in Russia are studded, while the share of friction tyres is about 30%.”

According to the Autostat estimates, tyre service centres account for more than a third of total tyre sales (including winter tyres), online retailers capture 28.1% of the market by offering lower prices thanks to zero rental costs, and non-specialised points of sale (markets, gas stations) take another 18.4% of the market. The remaining 19.4% of tyre sales are covered by private sellers.

Currently, the demand for auto chemicals and winter tyres has slightly picked up, however we do not expect major changes in the Russian market by the end of 2018.

Download PDF