Over the course of 2020, the oil and petrochemical industry was affected by a number of factors. SIBUR experts have collated and analysed the data in order to give a forecast of what to expect in 2021.

The pandemic continues: infections vs vaccinations.

By the end of 2020, the number of registered cases of novel coronavirus infections exceeded 30% of the actual estimated total. According to the analytics company Rystad, as at 12 January 2021, the actual number of people infected with COVID-19 stood at around 590 million people (7.7% of the global population), which is significantly higher than the official number of registered cases (92 million people globally). Despite the rapid deployment of vaccine production capacity, the number of cases will continue to grow in the first half of 2021: by the end of April it will have reached almost 880 million people (11.5% of the global population), with up to 3.8 million fatal cases.

Most regions will be able to vaccinate 75% of their populations by the end of 2021

Most regions will be able to vaccinate 75% of their populations by the end of 2021. Western Europe and North America will reach a 50% vaccination rate by the middle of the year, while East Asian and Middle Eastern countries will only reach this total by the end of 2022.

The global economy: growth after a fall

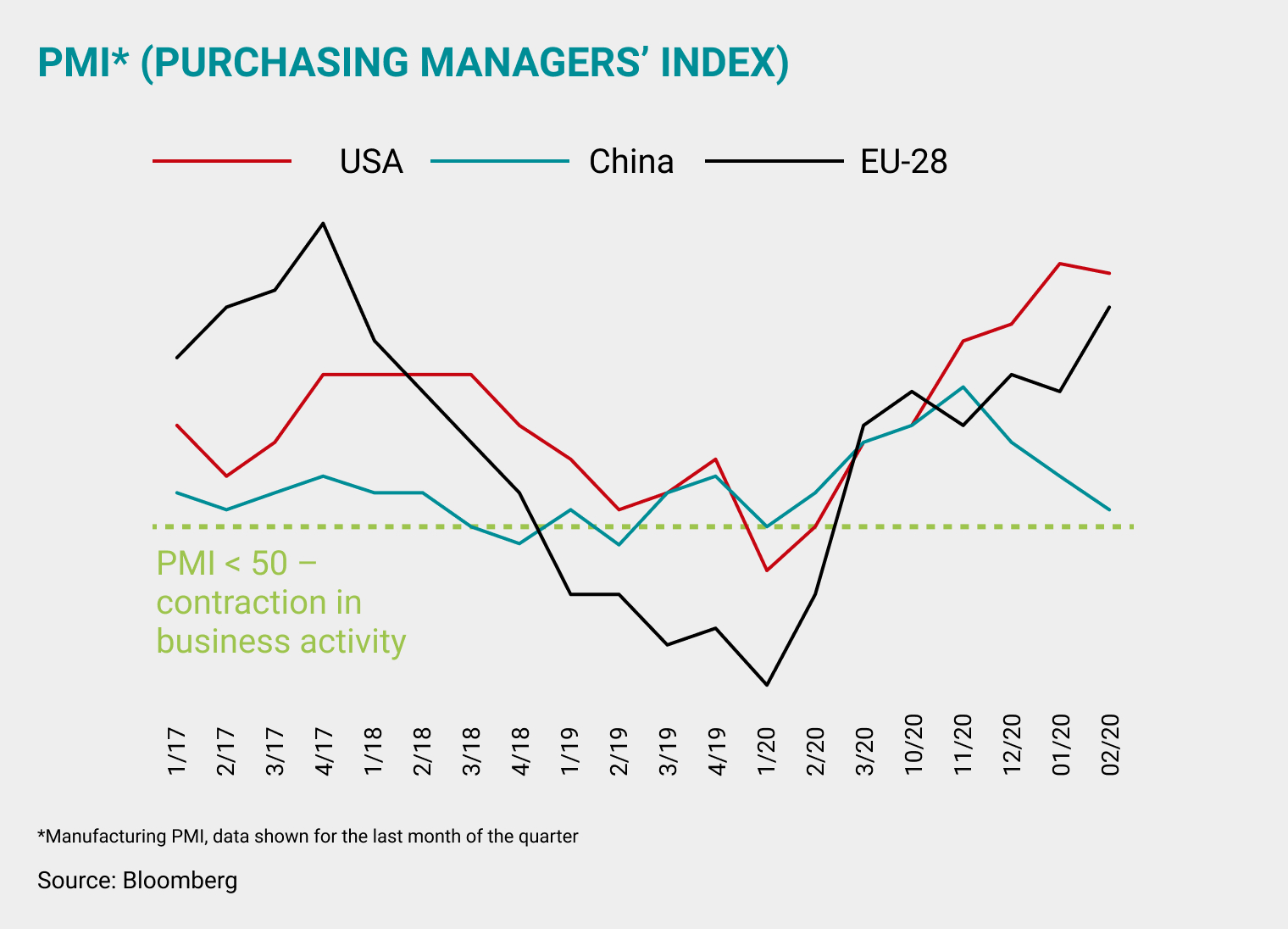

According to the most recent report by the International Monetary Fund, global GDP fell by 4.3% over 2020 (vs 2019). The US economy experienced a fall of 3.6%, and the European Union 7.4% (meanwhile, the Chinese economy grew by 2.6%). All the same, by the end of December the global economy had already begun to show signs of recovery. The Purchasing Managers’ Index (PMI) bears witness to the continuation of this trend, exceeding 50 points over the entire fourth quarter in the USA, China and EU.

Winter Storm Uri: the consequences for the petrochemical industry

On 15 February, Winter Storm Uri brought record low temperatures and record levels of snow to the USA, leaving millions of people without electricity. Oil and gas production suffered as a result, and the majority of petrochemical sites concentrated in Texas and Louisiana were forced to halt production. According to statements by the Oil & Gas Journal, citing ICIS and Genscape (a Wood Mackenzie subsidiary), around 80% to 90% of US olefin capacity was closed. According to an ICIS estimate, around 26 mtpa of ethylene capacity (67% of total US capacity) and 11 mtpa of propylene capacity (50% of total US capacity) had to be shut down.

According to the International Monetary Fund’s October 2020 estimate, global GDP shrank by 4.4% last year

Oil prices: raising forecasts

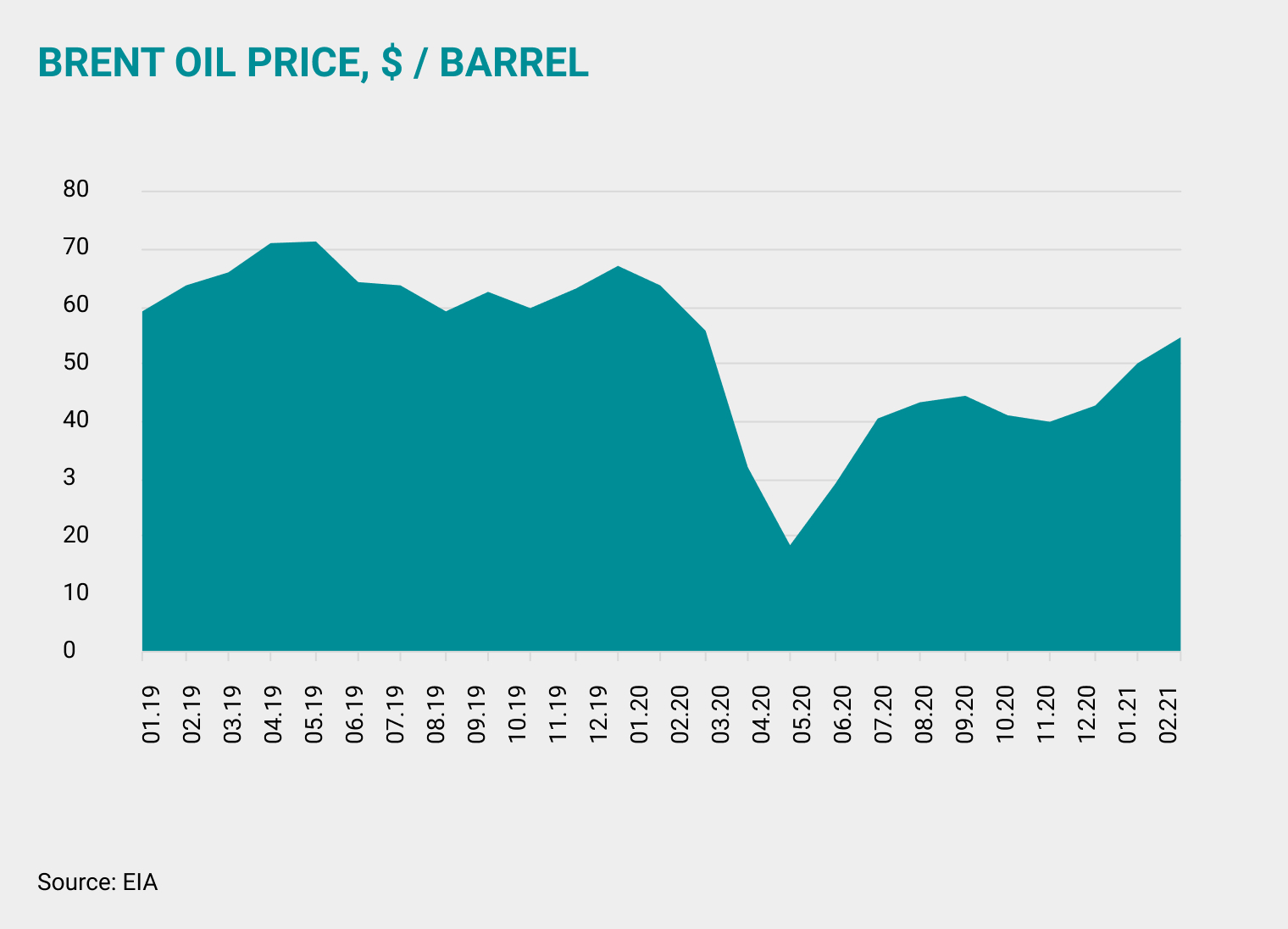

The average Brent price in Q4 2020 stabilised at USD 44 per barrel (demonstrating volatility in the range between USD 36 per barrel at the end of October and USD 52 per barrel at the end of December). While the demand for oil continued to recover, the rate of growth slowed due to new restrictions linked to curbing the spread of COVID-19. As a result, road traffic started to fall again in December: to 80% of pre-crisis levels in the USA, 60%–70% in Europe, and 80%–90% in Asia (according to Rystad).

In the second half of the year, the global market demand for oil exceeded current production, causing the significant inventories accumulated over the first half of the year to dwindle. In Q4, the OECD inventories of oil and petrochemical products exceeded the five-year average by 180 million barrels, or 6% (in mid-year, at the height of lockdown, it stood at 9%–10%, according to EIA).

Key OPEC+ producers met their production cut commitments. At the end of the quarter, oil prices rose on expectations of OPEC+ countries reaching an agreement on slower increases of oil supplies to the market. Following negotiations in December, the OPEC+ producers agreed to increase the common quota from 1 January by just 0.5 million barrels per day. At the start of 2021, Saudi Arabia committed itself to cutting production even further in February and March by 1 million barrels per day – to 8.125 million. This allowed the market equilibrium to be maintained, despite rapid growth in Libya to 1 million barrels per day during Q4 2020.

Major investment banks such as Barclays, Bank of America, Goldman Sachs and JPMorgan, are raising their forecasts for the average price of Brent crude. For example, JPMorgan raised its forecast for 2021 at the end of February to USD 64 per barrel (the previous forecast stood at USD 61 per barrel). The forecast for 2022 was upgraded by USD 6 to USD 72 per barrel. Barclays has raised its 2021 oil-price forecast for Brent crude by USD 7 to USD 62 per barrel. One of the main reasons for forecast revisions is the weaker than expected reaction of US producers to price increases and inventory normalisation following the exceptional snow storm in Texas.

The petrochemical industry: recovering demand

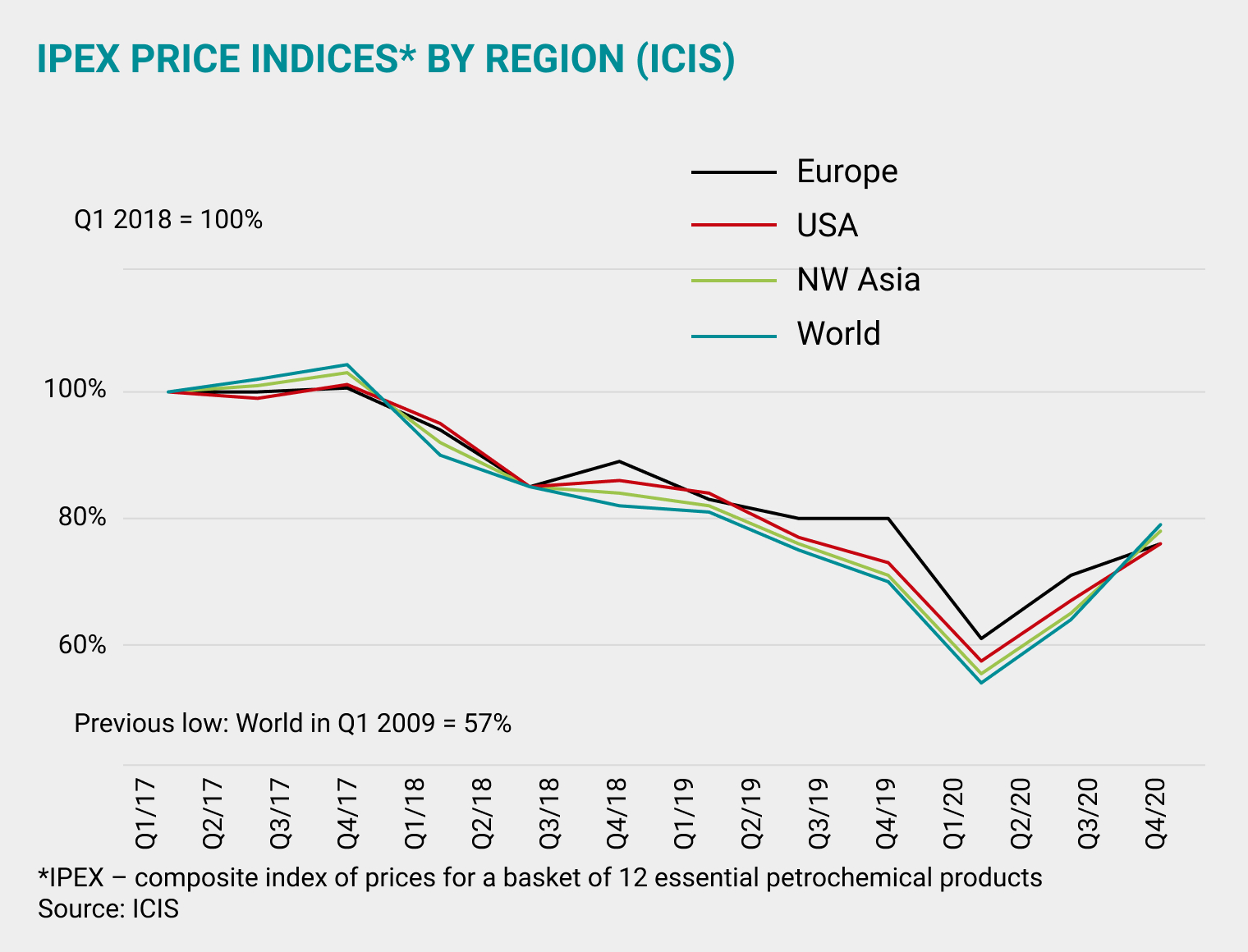

In Q4, prices for most petrochemical products recovered from the trough that began in March 2020. The IPEX index (a composite index of prices in key regions throughout the globe – North-East Asia, the USA, North-West Europe – for a basket of 12 essential petrochemical products: ethylene, propylene, benzene, toluene, paraxylene, styrene, butadiene, methanol, PVC, polyethylene, polypropylene, and polystyrene) grew by 9% quarter-on-quarter due to recovering demand, higher raw material prices and local supply shortages for certain products. Among high-tonnage products, the price of rubber increased markedly, following changes in butadiene prices. PET prices showed the least growth among the essential petrochemical products.

The automotive industry: a major fall

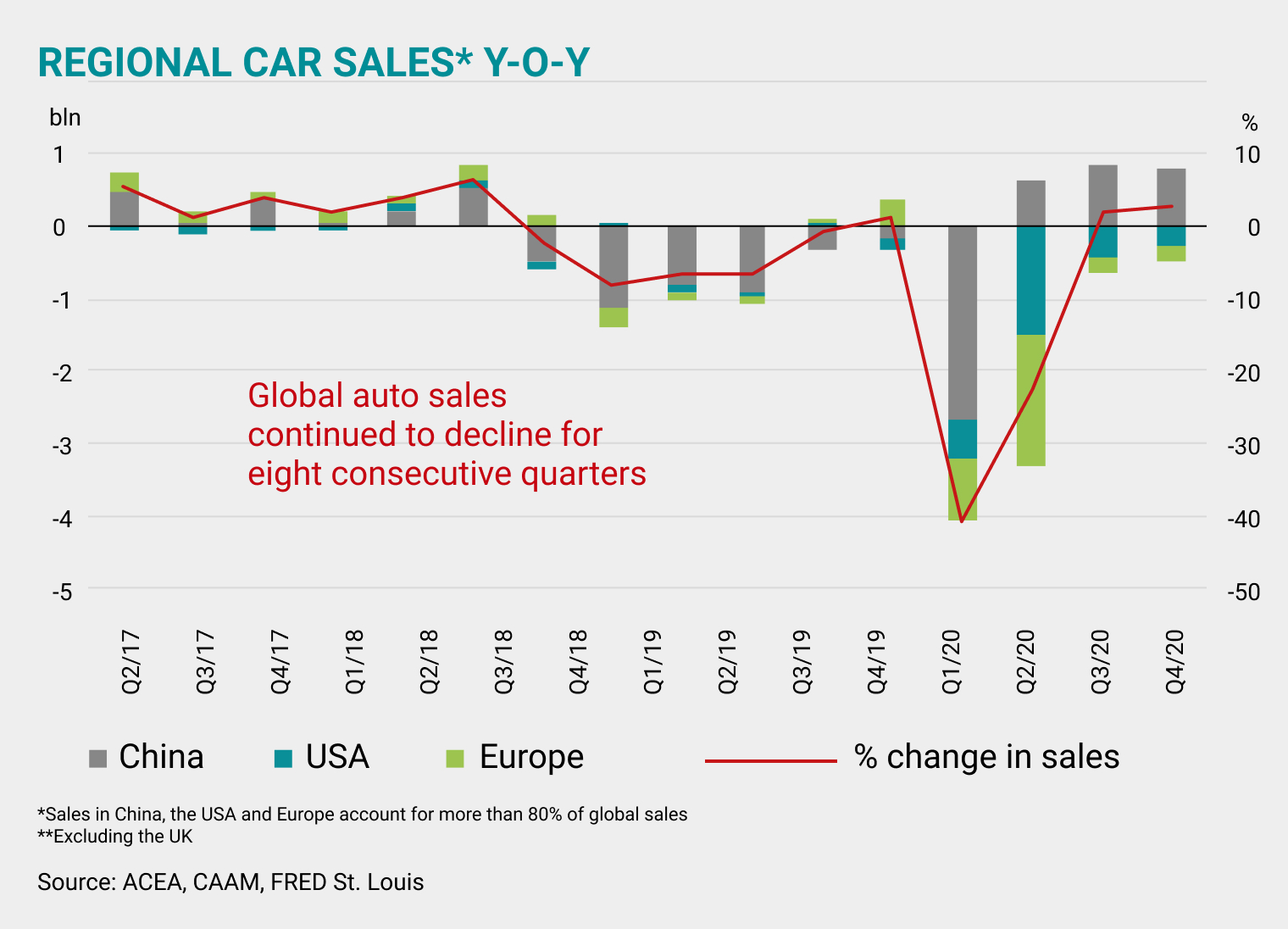

The automotive market deserves special attention, as this sector is a major consumer of petrochemical products. Over the course of the year, the market for passenger cars in the EU shrunk by 23.7% to 9.9 million units due to the pandemic. The number of new car registrations fell by 3 million from 2019. Over the year, car sales across all EU countries were in double-digit decline. Among the region’s major automotive markets, Spain experienced the sharpest drop (– 32.3%), followed by Italy (– 27.9%), France (– 25.5%) and Germany (– 19.1%). In China, car production and sales fell by around 2% year-on-year to 25 million units in 2020. Demand recovery was supported by the Chinese government subsidies for hybrid vehicle purchases and increased quotas for urban areas.

Major investment banks such as Barclays, Bank of America, Goldman Sachs, and JPMorgan, are raising their forecasts for the average price of Brent crude

PE and PP: new capacity additions

In Q4 2020, spot prices for PE in the core regions of Asia, North America, and Europe increased, which was also reflected in an increase in spreads from 12% to 22% (the difference in price quotations between PE and naphtha, its main raw material, in Asia and Europe, and between PE and ethane in the USA) and, as a result, production margins. The production issues that played out after Hurricane Laura in Q3 2020 caused the rise in prices in the USA.

New capacity additions continue to come on stream: the United States has seen the launch of Formosa Plastics and Sasol’s LDPE production plants, with a capacity of 400 ktpa and 420 ktpa, respectively. In China, Sinopec Zhongke Zhanjiang Petrochemical launched a 350 ktpa HDPE production project and Wanhua Chemical brought online 350 ktpa of HDPE and 450 ktpa of LLDPE. In Q1 2021, China’s Zhejiang Satellite aims to launch the country’s first ethane pyrolysis plant in Lianyungang, with a capacity of 1.25 mtpa. In preparation for its 400 ktpa of HDPE, the first deliveries of ethane from the US have already arrived.

An interesting development in the polyethylene market in the Q4 was the growth of HDPE and LDPE shipments to Asia from Iran, which were restricted from June to August amid US sanctions preventing a number of Iranian ships from entering Chinese ports for customs clearance. Supplies from Iran are increasing on the back of new capacity additions.

China is boosting its polyethylene capacities. Photo: Ding Lei/Xinhua/Zuma/TASS

Polypropylene spot prices also rose in Europe, China, and the USA. The spread between the price of the final product and the dominant raw material for its production (naphtha in Asia and Europe, propane in the USA) widened in all regions. The spread in the USA widened by 48% against the last quarter. This sharp increase was driven by the steady increase in domestic demand in Q4 being compounded by the unplanned closure of a number of facilities for repairs in December, paired with the fact that imports were unable to arrive on time. The increase in price quotations in China was driven by higher energy prices, the strengthening of the Chinese yuan against the US dollar and positive signals from the Chinese domestic market. China’s new stimulus plan to boost demand for cars, home furnishings and appliances is expected to drive demand for PP. Moving to Europe, Q4 prices were bolstered by a lack of supply following the shutdown of two PP production lines in France and a decrease in imports from the Middle East and Asia. Exports in the region remained stable.

Even despite COVID-19 and the increased attention it brought to hygiene requirements, the trend towards the use of recycled plastic is unwavering, and large companies have not abandoned their goals of swapping out virgin pellets for recycled ones

As with the PE market, the launch of new PP production capacities continued into Q4: in China, Sinopec Zhongke Zhanjiang Petrochemical opened a new plant with a capacity of 200 ktpa, and Wanhua Chemical brought 300 ktpa of capacity on stream.

PET: the transition to recycled

Polyethylene terephthalate (PET) prices were much more sluggish to respond to Q4’s recovery in economic activity. Compared to the previous quarter, the increase in price quotations in Asia and Europe did not exceed 3%. The main drivers behind this were low seasonal demand and, as with other products, a shortage of containers for imports from China. In certain instances, this situation has led to a three to fivefold increase in the cost of transportation and longer delivery times.

In Europe, a slight increase in quotations for virgin PET has propped up a high premium on recycled pellets against virgin pellets: it has exceeded USD 700 per tonne since Q2 2020. COVID restrictions on the collection of plastic waste for recycling have driven up this premium.

However, even despite COVID-19 and the increased attention it brought to hygiene requirements, the trend towards the use of recycled plastic is unwavering, and large companies have not abandoned their goals of swapping out virgin pellets for recycled ones. PepsiCo, for example, is switching to fully recycled polyethylene terephthalate (R-PET) in nine European countries, reducing its virgin PET consumption by 70 ktpa. Germany, Poland, Romania, Greece, and Iceland will make the switch in 2021, with France, the UK, Belgium, and Luxemburg following in 2022. Another ripple of companies committing to this switch is the increase in SUEZ and LyondellBasell’s market share for recycling. Tivaco, whose production is based in Belgium, was acquired by LyondellBasell and SUEZ, who plan to integrate it into their Quality Circular Polymers (QCP) joint venture. Thanks to the deal, QCP’s recycling capacity will increase to approximately 55 ktpa, as the Tivaco plant boasts five production lines capable of processing 22 ktpa.

Many European countries and major companies will make the switch to recycled PET in 2021.

In Q4, prices for most petrochemical products recovered from the trough that began in March 2020

Rubbers: “natural” support

The price of butadiene continued to rise throughout the quarter, but it came to a halt by the end of December for several reasons. Firstly, consumers expected the launch of the new Chinese steam crackers at the beginning of Q4, while the capacity only actually came on stream towards the end of the quarter. For this reason, Chinese buyers’ stockpiles of butadiene started to dwindle, driving buy-side pressure. Secondly, spring 2020 brought an unscheduled steam cracker repair in South Korea, which temporarily reduced supply before production resumed in early December. Thirdly, the ongoing increase in the price of natural rubber since the beginning of October has provided strong support to prices in the synthetic rubber and butadiene market.

Spot prices for eSBR also grew in Europe and Asia. Several factors coalesced to drive a sizeable increase in the Asian quotation (about 50% more than the previous quarter), including car production picking back up and, as a result, the replenishment of tyre stocks. In Asia, the natural rubber market also saw a sharp increase in quotations. The key drivers behind this are increased demand from China, lower production in Thailand amid a COVID-related lack of workers coming from Laos and Myanmar, and a fungal disease ripping through rubber trees in South-East Asia.

Download PDF