SIBUR Integrated Management System tested successfully

External surveillance audit of SIBUR Integrated Management System completed at the end of April.

SIBUR at IPTF. New grades and services

The 10th Anniversary International Polymer Technology Forum (IPTF) was held on May 17-18 in St. Petersburg.

AGCC construction is underway

With the readiness of the Amur Gas Chemical Complex nearing 40%, the project implementation strategy will be updated.

First batch of MAN produced by SIBUR

This will make it possible to fully meet the domestic demand for MAN in 2022.

SIBUR will host a webinar "Ensuring company's stability in the new framework"

Join us on April 12th at 11:00 Moscow time.

SIBUR for Clients is having a shake-up!

We are updating the SIBUR for Clients magazine to make it a more interesting, useful, and insightful publication for our readers.

SIBUR streamlines supplies

From 1 March, products made by our Kazan and Nizhnekamsk sites can be purchased through our one-stop shop platform.

Polyethylene from ZapSibNeftekhim: even more premium grades

ZapSib is set to launch high-density polyethylene production using suspension polymerisation in a move that will further expand its product mix.

SIBUR teams up with Samruk-Kazyna and KazMunayGas

An important agreement was signed at Eurasia’s 14th KAZENERGY Forum.

SIBUR features on the TV channel Nauka 2.0

Employees from SIBUR PolyLab shared their experience creating polymers containing recycled materials.

NKNKh: winning an enviromental award

Nizhnekamskneftekhim’s systematic approach to environmental protection was highly rated by experts.

SIBUR updates its 2025 ESG Strategy

In November 2021, SIBUR’s Board of Directors approved changes to the 2025 Sustainability Strategy.

Kazanorgsintez receives Government Prize for Science and Technology

The enterprise was recognised for its polycarbonate production technology.

The Nobel Prize in Chemistry 2021

Benjamin List and David MacMillan were awarded the Nobel Prize in Chemistry 2021 for the development of asymmetric organocatalysis.

Introduction to ESG

Sberbank Corporate University has made its new ESG: Introduction training course available free of charge on its website.

Competitive advantages of SBS

Voronezhsintezkauchuk: helping manufacturers of adhesives.

Russian SBS polymers for the road building industry

Review of Russian road building industry and SIBUR’s SBS development.

More flexible, more agile, more efficient

Base Polymers Division of SIBUR — regarding the results of SIBUR and TAIF assets consolidation.

Global Plastics Outlook until 2060

Three development scenarios in the new report by OECD.

Action plan for managing accounts receivable

Get the receivables under control.

SIBUR and TAIF: first results of integration

A commitment to stability, regional development and environmental protection.

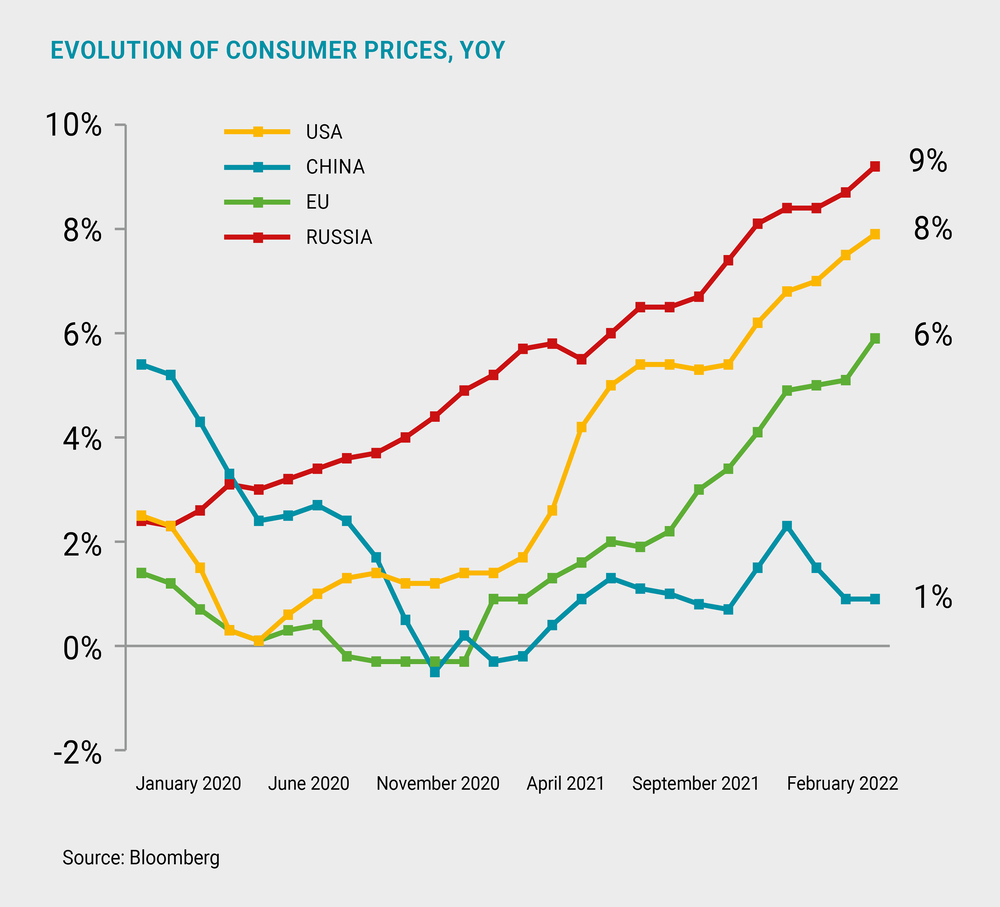

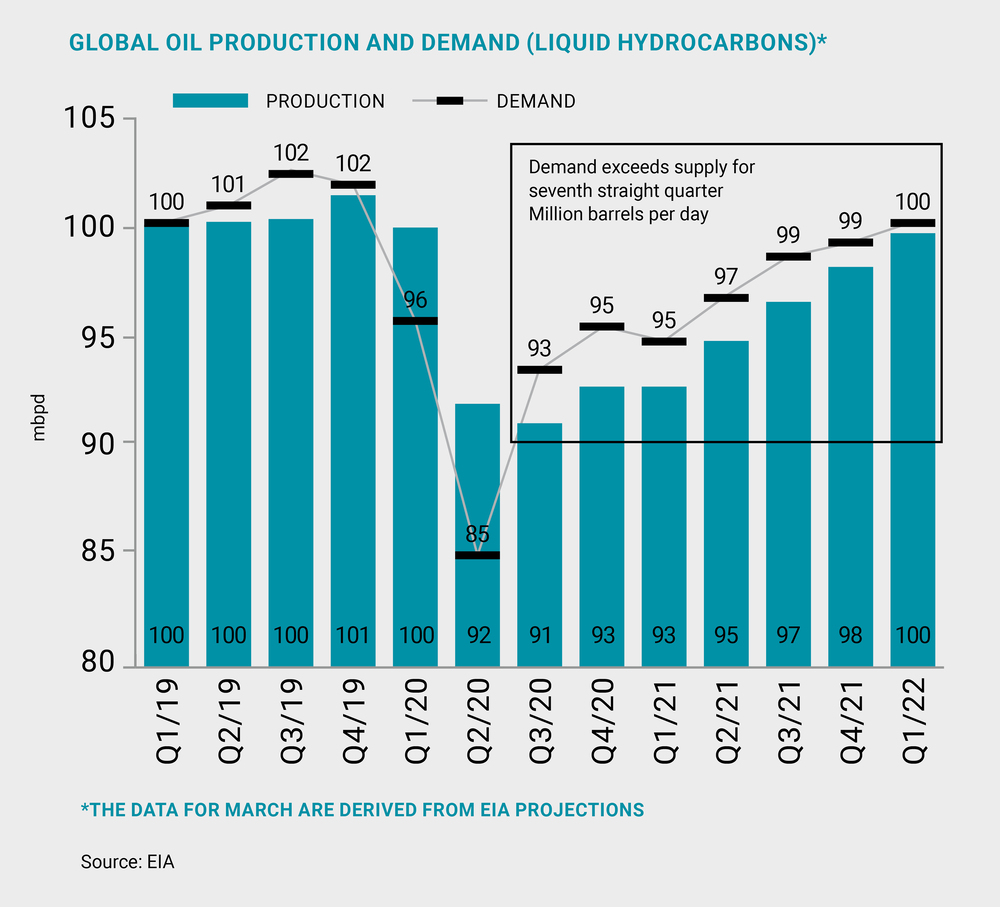

Petrochemicals in facts and figures

Inflation breaks records, oil in deficit for the seventh consecutive quarter. What's next?

Green insulation from the air

Expandable polystyrene: unlocking new business development opportunities.

EKONS ‘in business’

SIBUR staff members discuss how EKONS contributes to the holding’s digital transformation.

Petrochemicals in facts and figures

The economy is recovering from the initial shock of the pandemic, but there are still headwinds.

Why are polymer pipes eco-friendly?

At every stage of the life cycle, they reduce greenhouse gas emissions.

Where the olefins and polyolefins markets are headed in 2022

Wood Mackenzie experts highlight key trends.

Petrochemicals in facts and figures

Could inflation continue to grow throughout 2022, and will it lead to shortages? Here is what experts from SIBUR’s Investment Planning and IR have to say about it.

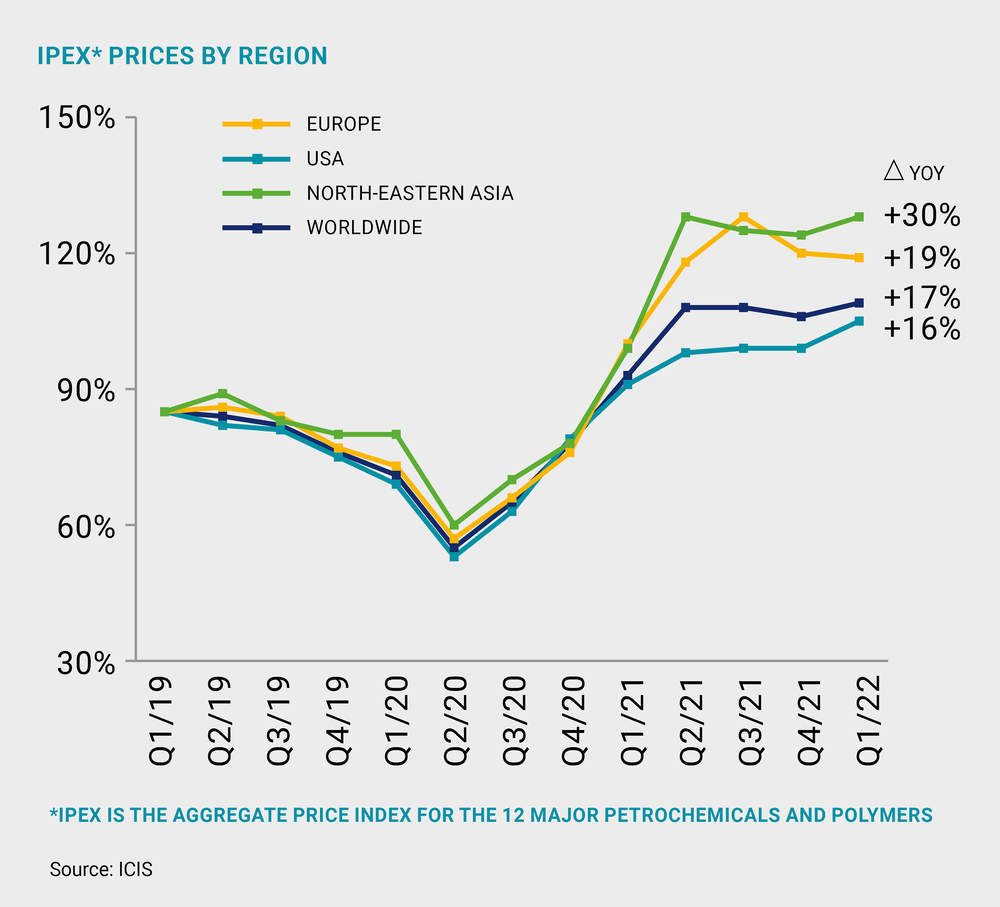

Polymer Prices

After a long rally, a fall, then a bounce? How oil prices will change and how adjacent markets will react.

Macroeconomics in Russia

Soaring gas prices could result in between USD 20 billion and USD 100 billion in extra revenue for Russia in 2022.

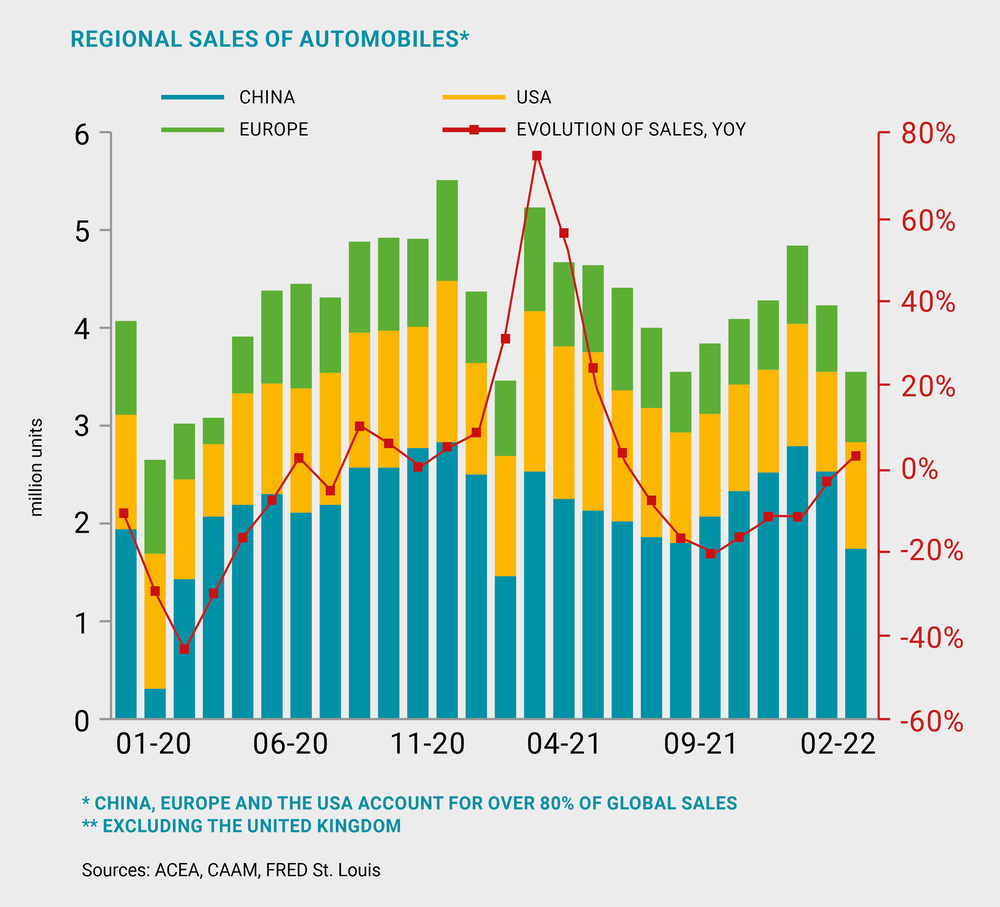

SIBUR shifts to industrial sales

The new sales principle brings benefits not only for clients, but also for the entire industry.

Recycling projects

SIBUR’s progress on teaming up with partners to implement recycling and circular economy initiatives.

Vivilen – a ready-to-use ESG solution

Vivilen, a compound made using recycled polymers and developed by SIBUR is now being used in PPG Tikkurila paint packaging.

EKONS: visible savings

Visualising operational metrics has saved SIBUR about RUB 3 billion since 2018.

"No reason for pessimism ahead"

CEO of Gazpromneft - Bitumen Materials Dmitry Orlov talks about the common ground between petrochemical and bitumen producers.

Gotek-Polipak: 30 years in business

Aleksey Dunat, Director at Gotek Polipak, spoke to us about setting a benchmark for other companies in the industry.

KAPITEL IRKUTSK SECRETS OF SUCCESS

Pyotr Kraykovsky, CEO and Chief Process Engineer of Kapitel Irkutsk, talks about how the company became a manufacturer of unique materials.

"A focus on unique solutions"

Yuri Kazantsev, Head of Diesel Additives at Oduvanchik, spoke to us about how his company went from a trader to a leading regional manufacturer.

"We made the right choice"

We spoke to Dmitry Kochergin, Commercial Director at SLT Aqua, about how his company forges relationships with partners.

Being prepared for any changes

Marina Medvedeva, Member of the Management Board – Managing Director at SIBUR, talks to us about her choice of path in life, love of collecting, and drive.

Building a more skilled postpandemic workforce

McKinsey experts discuss how companies are preparing employees for the global changes brought on by the COVID-19.

Internet marketing for an industrial brand

How being transparent and interactive helps drive customer loyalty and attract new business.

"A thought that spurs on change"

Maria Lukyanova, T&D manager, psychologist, and a speaker on the SIBUR Business Practices platform, talks to us about the secrets of learning successfully.

TOP MANAGERS TAKING QUESTIONS

In the Q&As section, our top managers answer the most interesting and relevant questions from our clients sent to dearcustomer@sibur.ru.